The ocean freight market is heading into a summer where the headline story and the real story diverge sharply.

Rates are moving higher, with bunker surcharges of around USD 500 per FEU entering July pricing, and the unresolved uncertainty surrounding the Strait of Hormuz reinforcing expectations of a prolonged period of disruption. At a Xeneta-hosted NYC Freight Roundtable on June 4, participants described a growing consensus that disruption is unlikely to ease before Q3 at the earliest, with many planning as if it will last through the full contract year. As Peter Sand observed, "The wave of freight rate increases is gathering momentum."

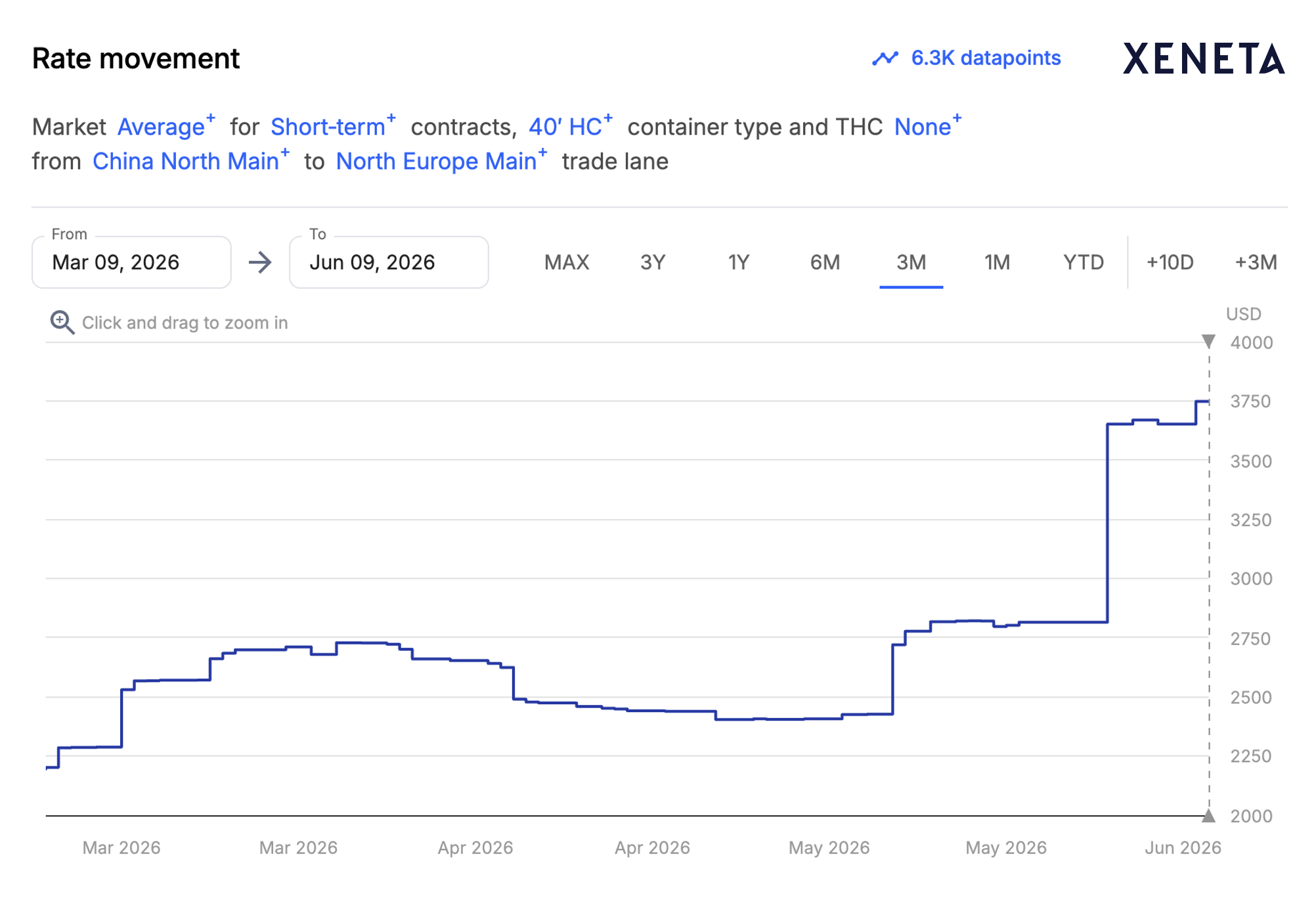

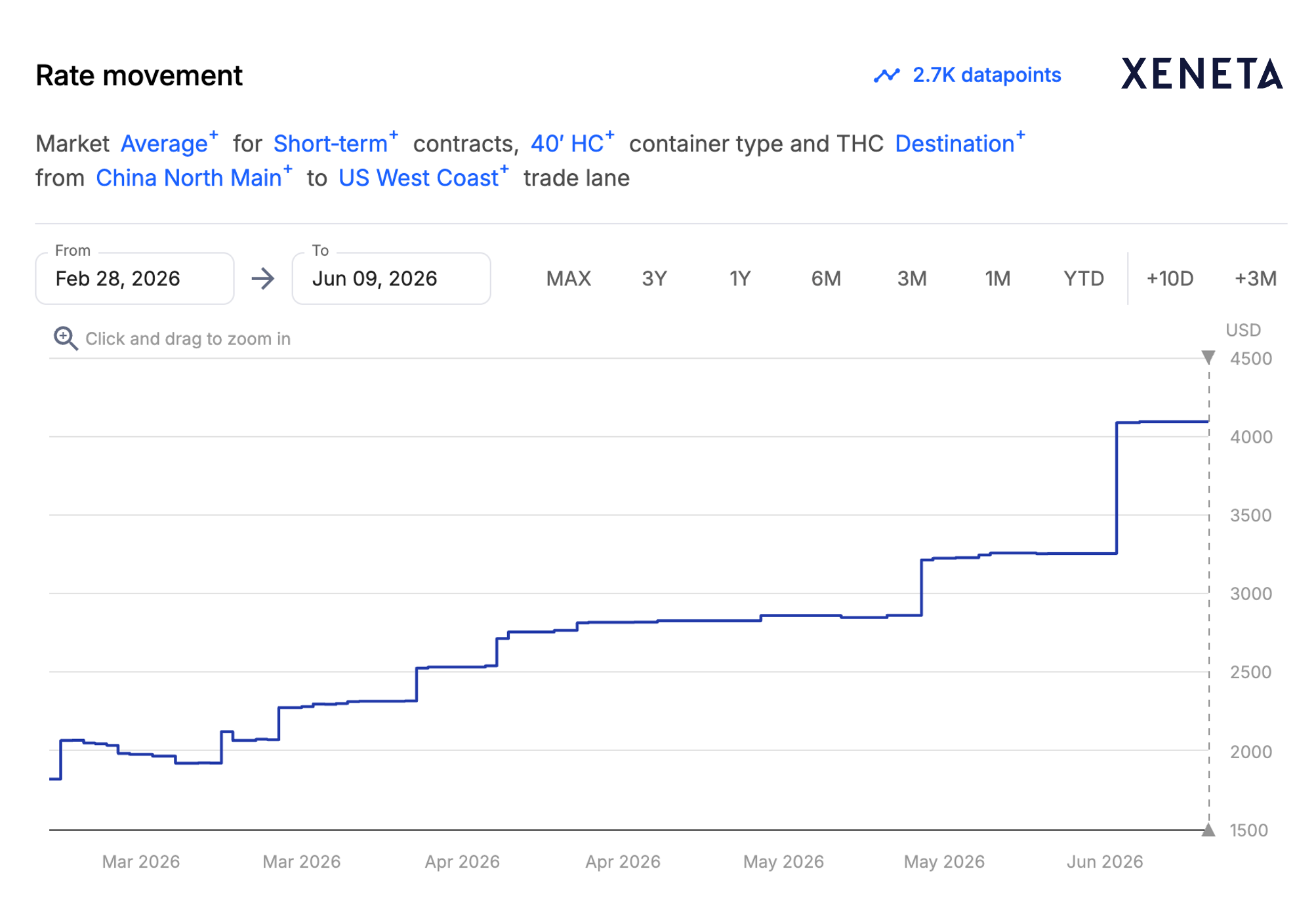

And spot rates tell the same story: the cost of a 40-foot container from Asia to northern Europe hit $3,649 as of June 6 — a 27% jump in a single week — while the Asia–US West Coast rate rose 20% to $3,933, according to Xeneta data cited in Bloomberg on June 7.

On the surface, this looks like a strong (if early) peak season.

But the volume behind those rates tells a different story.

The demand is borrowed, not generated

Carriers, forwarders, and logistics managers across the industry describe the same pattern: demand is being pulled forward into June rather than generated organically through a traditional peak cycle.

That frontloading is itself driving part of the rate surge. "If shippers do look to frontload imports, then carriers will look to push rates higher and higher, so the market may yet be far from its peak across trades globally," Peter Sand, Xeneta's chief analyst, told Bloomberg on June 7.

The risk is that today's elevated rates may be masking weaker demand ahead. If imports continue to be pulled forward at the current pace, August volumes could fall well short of what July's pricing would imply, leaving companies that plan against current rate signals exposed to inventory imbalances and inaccurate cost forecasts.

That view is supported by forecasts from the National Retail Federation and Hackett Associates, which expect US container imports to remain below 2025 levels into early fall despite a temporary year-over-year increase in May and June. Their conclusion is similar to what carriers and shippers described at the roundtable: near-term volume strength reflects timing effects and disruption, not a broad-based acceleration in demand.

Rates and fundamentals are not aligned

This divergence is not new. Xeneta data has highlighted it throughout this year's contract negotiations. Despite elevated spot rates driven by Middle East disruption, shippers negotiating long-term agreements continued to secure rates below prevailing market levels. In other words, carriers were competing aggressively for committed volume even as spot prices climbed.

Short-term rates from China North Main to the US West Coast have risen 125% since the conflict with Iran began on February 28, while rates to northern Europe are up more than 50%, according to Xeneta. Those increases reflect disruption, rerouting costs, and fuel surcharges far more than any meaningful shift in underlying demand.

Some of the recent strength may also reflect shippers accelerating imports ahead of bunker adjustment factor (BAF) increases scheduled for July 1, adding another layer of frontloaded demand to the market.

Port disruption is compounding the pressure. Shipments rerouted around the Strait of Hormuz are causing congestion at Southeast Asian transshipment hubs including Singapore and Malaysia's Port Klang. "Port disruption is toxic for supply chains, especially at transshipment hubs with global significance in Southeast Asia," Sand said in Bloomberg. "So this is driving massive market spikes on trades such as the transpacific which does not transit the Middle East."

Some operators are also beginning to monitor secondary effects of prolonged vessel delays in Gulf waters, including hull fouling and maintenance requirements that could reduce vessel efficiency even after normal transit patterns resume.

Taken together, the evidence points to a market where freight rates are being driven primarily by disruption and timing effects rather than a broad-based surge in cargo demand.

Reliability is now the procurement conversation

Rising rates would be easier to accept if service were improving. It is not.

Global schedule reliability is running in the 35-40% range across most trade lanes. One large multinational shipper described adding seven days to every transit-time forecast as standard practice. Roundtable participants agreed: reliability is now driving more procurement decisions than price.

One major chemical manufacturer used Xeneta reliability benchmarks during carrier negotiations for the first time this year. The data resolved disputes over carrier performance claims that had previously consumed weeks of back-and-forth. The result was first-round bid savings of 25-30% versus the prior year.

Relationships + realtime data are now the competitive edge

When capacity tightens, carriers allocate space to customers they trust — and that trust is increasingly built on data. Multiple carriers at the roundtable acknowledged maintaining internal assessments of shipper behaviour. Customers with accurate forecasts and a track record of honouring volume commitments are more likely to secure space when markets tighten.

The data advantage runs both ways. One leading e-commerce platform operates on a rolling six-week forecasting cycle, sharing projected volumes with carriers continuously rather than only during annual tenders. The result is fewer cargo rollovers and more reliable access to capacity. A global fashion company described a similar approach, crediting ongoing carrier conversations grounded in real shipment data for maintaining access during previous periods of disruption.

The common thread among the companies navigating this market most effectively is not negotiating leverage. It is visibility. They know their numbers, share them proactively, and enter discussions with carriers armed with evidence rather than assumptions. In a market where rates are rising but fundamentals remain uncertain, that discipline creates a meaningful advantage.

What the next six weeks will reveal

Several forces are converging simultaneously:

-

Frontloading continues to pull cargo into June

-

Bunker surcharges are entering July pricing

-

Middle East disruption keeps carrier costs elevated

-

Schedule reliability limits effective capacity

- Underlying demand growth remains modest, with NRF forecasts pointing to import volumes remaining below 2025 levels through early fall despite a temporary June increase.

Collectively, these conditions could push freight rates higher even as underlying shipment volumes begin to soften. That is the central tension in today's market: pricing signals strength, while many of the underlying indicators point to disruption-driven demand being pulled forward rather than sustained growth.

For carriers, the coming weeks may look like a strong summer. For shippers managing inventory, procurement, and transportation budgets, the picture is considerably more complex.

Xeneta's mid-year ocean and air freight outlooks – due in the coming weeks – will provide a clearer view of how rates, reliability, and capacity are evolving as the market enters the second half of the year. For shippers assessing carrier performance, benchmarking contract rates, or preparing for July pricing changes, it should prove timely reading.

Request early access to the mid-year outlooks.

.png?width=387&name=freight-ship-reliability%20(1).png)