Latest data shows containerized imports into the Middle East collapsed in the month immediately following the escalation of conflict at the end of February, down 64% in March year-on-year. Exports from the region were down 62% year-on-year.

The data, released by Xeneta and Container Trades Statistics this week, is the clearest sign of the magnitude of the disruption and the importance of the Strait of Hormuz for container trade in the Middle East, essentially cutting off a seaborne trade artery into critical ports such as Jebel Ali and Khalifa in UAE, Dammam in Saudi Arabia and Hamad in Qatar.

If this sudden collapse in trade in the Middle East acted as the initial earthquake, the aftershocks are still spreading across global supply chains. This wave pattern means it is not always easy for supply chain professionals to provide credible explanations internally to finance teams on why the freight budget has been blown apart – and, perhaps more importantly, what the forecast is for the remainder of 2026. This is especially the case if you are not shipping on trades directly impacted by the Strait of Hormuz.

This blog will provide clarity and key considerations for the remainder of 2026.

Note: ‘Middle East’ includes Iran, Iraq, Kuwait, Saudi Arabia, UAE, Qatar, Bahrain, Oman, Yemen, Jordan, and Egypt (Ain Sokhna only).

Waves of disruption

We are now three months into the Middle East conflict and a familiar wave pattern is emerging.

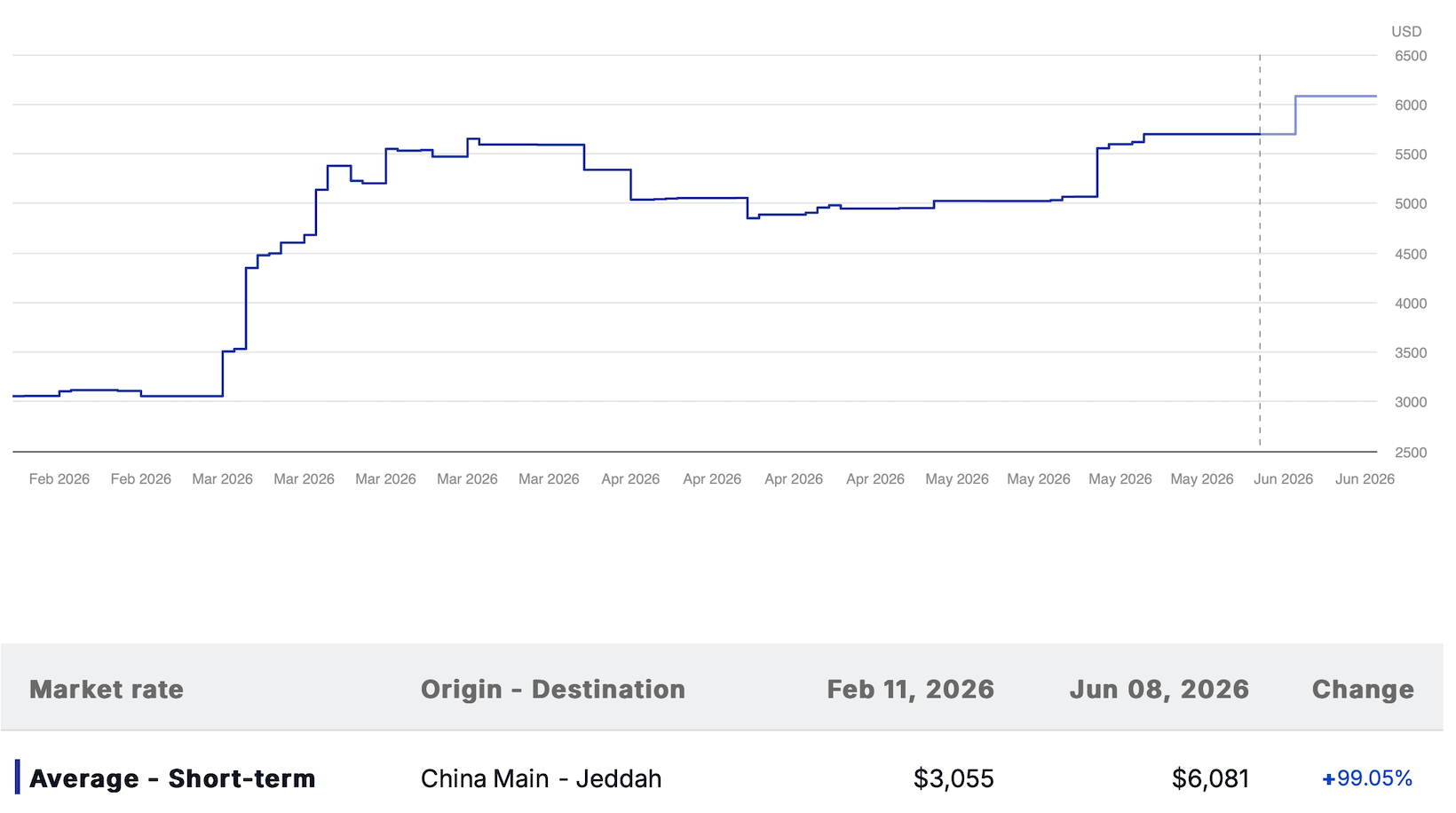

Port of Jeddah is a good example because it is acting as the gateway to a land bridge into areas of the Middle East cut off by the Strait of Hormuz.

Between 28 February (date of escalation in conflict) and 22 March, average spot rates from China to Jeddah increased 85%.

While this is not too surprising, what causes more confusion is spot rates then began to ease slightly, falling back 14% by 15 April.

If this lulled procurement professionals into telling finance colleagues they were through the worst, it was a mistake. Since then, a second wave has hit, with average spot rates already spiralling past the 22 March spike and expected to rise to around 100% above pre-conflict levels at the start of June.

History lesson in freight rate spikes following black swan events

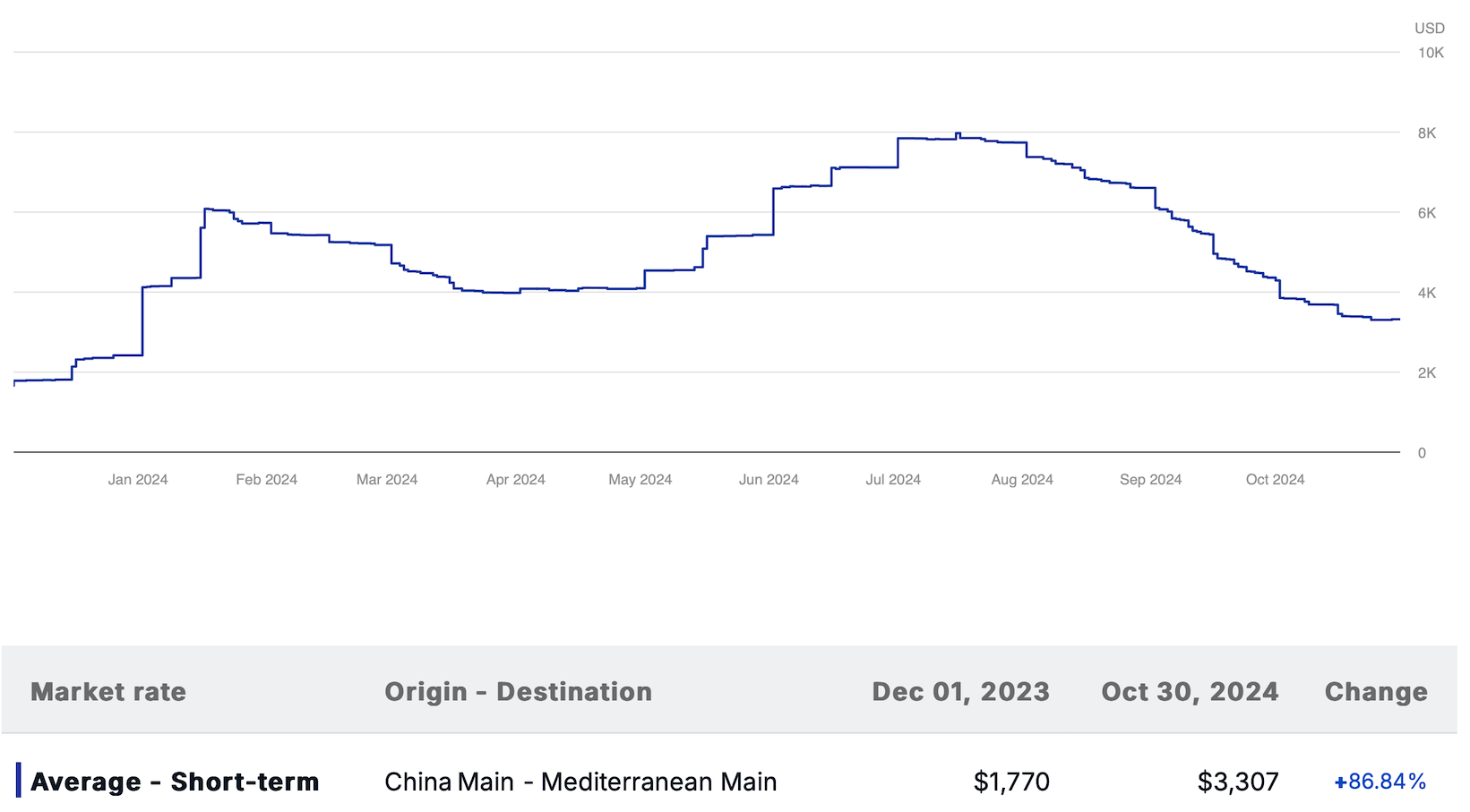

The wave effect is a familiar pattern during a black swan. Following the escalation of attacks by Houthi Militia in the Red Sea in December 2023, average spot rates from China to Mediterranean increased 243% by 16 January 2024 (compared to 1 December), before falling back 35% by 30 March (from the mid-Jan spike).

Again, if a procurement professional told their senior management or finance team the worst was behind them, it was a big mistake. From that point, average spot rates spiralled upwards and didn’t peak until 15 July 2024 when they hit 350% above pre-conflict levels (1 December 2023). It then took six months for rates to fall back to the 30 March level – a much sharper rise than the fall.

If you are struggling to explain the financial impact of the latest Middle East crisis to your Chief Finance Officer, understanding these patterns provides credibility in a seemingly chaotic environment.

If history is anything to go by, the second wave of rate increases on the trade from China to Jeddah are likely to climb even higher. It should certainly not be ruled out and is important to flag with finance teams already reworking freight budgets for the remainder of 2026.

Waves rippling across global trades

If you are shipping on a trade into the Middle East, the explanation for increased freight costs is easier. But what if you are shipping on a trade thousands of miles away on the Transpacific from China to US West Coast? How do you explain to the Chief Finance Officer that average spot rates are set to be more than 80% higher at the start of June compared to pre-conflict in February?

We can also see the wave pattern on the Transpacific trade. There was a modest 12% increase in average spot rates on 1 March before easing back 8% by 14 March.

Perhaps the Transpacific was insulated from the impact of the Middle East crisis given it is nowhere near the epicenter of conflict? Again, this is an error.

The second wave has now hit the Transpacific, with average spot rates from China to US West Coast expected to reach 84% above pre-conflict levels in June.

Strategies for the remainder of 2026?

There is no hiding place from the disruptive impact of the closure of the Strait of Hormuz and sudden collapse of trade into the Middle East.

Compared to pre-conflict, average spot rates in June are expected to be +75% from China to US East Coast, +51% to North Europe, +45% to Mediterranean and +57% on the Transatlantic from North Europe to US East Coast.

Some shippers have delayed signing new long term contracts on major fronthaul trades in the hope spot rates will begin to ease and give them a stronger negotiating position. The false dawn of easing spot rates following the first wave could have encouraged this wait-and-see approach.

However, given the second wave of rate increases is now seen across major trades, continuing to play on the spot market could be a dangerous game.

A shipper will be reluctant to lock into a long term rate that is higher than they budgeted for at the start of the year, but it may be the least worst option and at least provides some clarity for finance teams in understanding full year cost impact of the Middle East conflict.

If you are a procurement professional facing this dilemma, whatever strategy you adopt for the remainder of 2026, you can provide credible explanations and rationale for your decisions though Xeneta data and market intelligence.

Index-linked contracts are a strong option

No one has a trustworthy crystal ball and, given the highly-volatile geopolitical situation, nothing should be ruled out in 2026 and beyond.

That is why many shippers are adopting index-linked contracts, where the rate paid tracks the market against agreed parameters with the service provider.

This does not fully insulate a shipper from the waves of freight rate increases following a black swan, but it offers many benefits.

Firstly, it is likely the index-linked rate will be below the price a shipper would pay on the spot market.

Secondly, it gives the shipper a level of assurance that, should the situation improve in the Middle East and freight rates begin to soften, they will not be locked into paying an uncompetitive rate in a traditional long term contract agreement.

Additionally, an index-linked contract provides greater certainty the shipper’s cargo will make it onboard the ship, while forwarders and carriers both also benefit from this type of agreement. During uncertain times, index-linked contracts support buyers and sellers of freight to work in partnership.

What Shippers Should Do Now

There are three things every shipper should be doing in this environment, regardless of whether their cargo touches the Middle East.

-

Get the data to explain the situation internally. Finance teams and senior management are asking why freight budgets are broken. Having lane-level rate benchmarks and market context to hand is the difference between a credible explanation and a shrug. If you cannot explain what the market is doing and why, you cannot make the case for the budget you need.

-

Reassess your exposure to the spot market. Shippers who delayed signing long-term contracts in the hope that rates would soften have found themselves increasingly exposed to a spot market that is still rising. Long-term contract rates carry a discount to the spot market and provide predictability. Index-linked contracts go further, aligning your rate to market movements while removing the risk of being locked in above-market if conditions improve (or not getting any space onboard the ship if rates rise).

-

Look beyond the rate. Cancellation rates, schedule reliability, and actual versus announced transit times vary significantly by carrier and corridor right now. Paying a lower rate for a service that cancels or delivers three weeks late is not a saving it’s another (potentially self-inflicted) disruption. Carrier performance data — not carrier promises — should drive routing decisions.

.png?width=387&name=freight-ship-reliability%20(1).png)