The Xeneta Weekly Ocean Container Shipping Market Update provides data and intelligence including the latest freight rate and capacity movements across global trades with supporting insight from Peter Sand, Xeneta Chief Analyst.

Xeneta analyst insight

Peter Sand, Xeneta Chief Analyst:

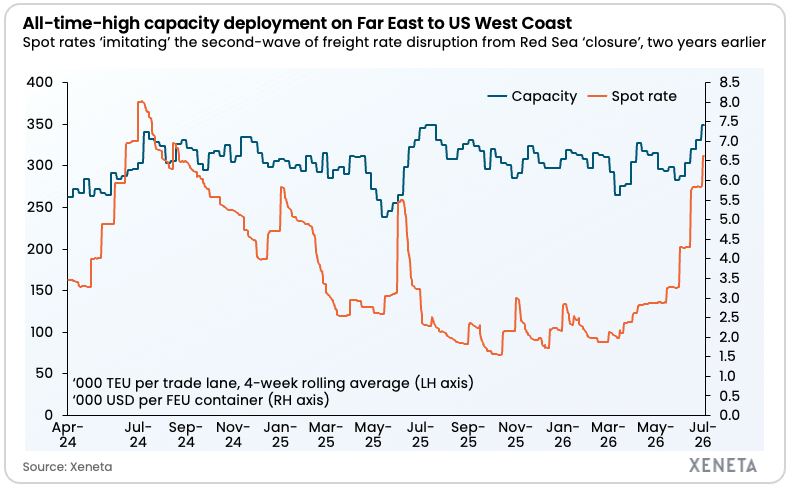

“Ocean container shipping is running hot on the Transpacific, with offered capacity from Far East to US West Coast hitting an all-time high this week and spot rates showing another double-digit increase to now sit +253% compared to pre-Strait of Hormuz crisis at the end of February.

“The combination of record capacity deployment and further rate increases on the Transpacific tells us demand is strong and that carriers are scrambling to satisfy it.

“Double-digit spot rate increases are seen across all major fronthauls from Far East to US and Europe in a clear sign peak season is already here at a global level. Shippers are moving right now to bring goods out of Asia and get them where they need to be ahead of potential further disruption during the peak season and a backdrop of continuing uncertainty in the Middle East.

“The four-week rolling average for the week commencing 29 June stands at approximately 350 000 TEU on the Transpacific to the US West Coast – matching the previous record of around 349 000 TEU set in the wake of the 90-day US tariff pause in early July last year.

“Xeneta data shows carriers are adding capacity fast. MSC reinstated the Pearl-service on 13 June, with the MSC LYSE V the first vessel to call at Long Beach on Tuesday 30 June. Yang Ming and ONE are also running extra-loaders.

“However, our expectation is that the market is not ready to turn a corner just yet with spot rates continuing to rise into mid-July at least on the major fronthauls to Europe and US. More capacity is welcome and will help shippers to move goods more reliably, but it is not enough to reverse the upwards trend.”

Data highlights

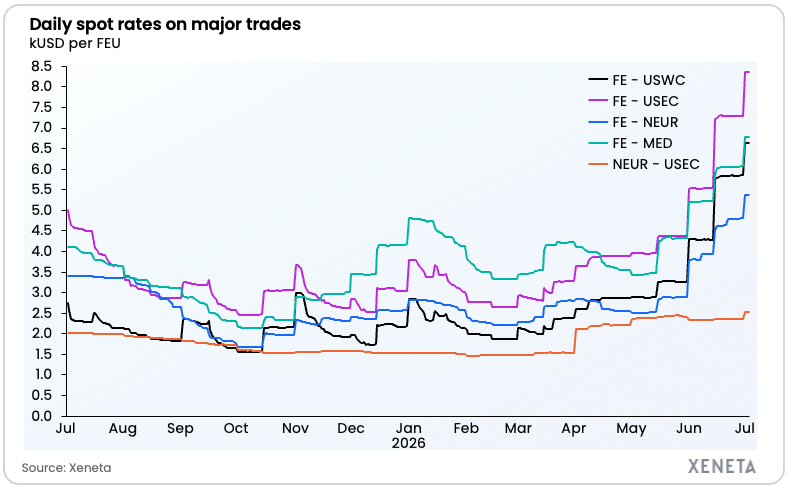

Market average spot rates – 3 July 2026:

-

Far East to US West Coast: USD 6 639 per FEU (40ft container)

-

Far East to US East Coast: USD 8 362 per FEU

-

Far East to North Europe: USD 5 377 per FEU

-

Far East to Mediterranean: USD 6 772 per FEU

-

North Europe to US East Coast: USD 2 523 per FEU

Spot rate changes over the past week – 3 July vs 26 June 2026:

-

Far East to US West Coast: +14%

-

Far East to US East Coast: +15%

-

Far East to North Europe: +13%

-

Far East to Mediterranean: +12%

-

North Europe to US East Coast: +7%

Spot rate changes since the end of February (pre-crisis) – 3 July vs 28 February 2026:

-

Far East to US West Coast: +253%

-

Far East to US East Coast: +215%

-

Far East to North Europe: +142%

-

Far East to Mediterranean: +103%

-

North Europe to US East Coast: +71%

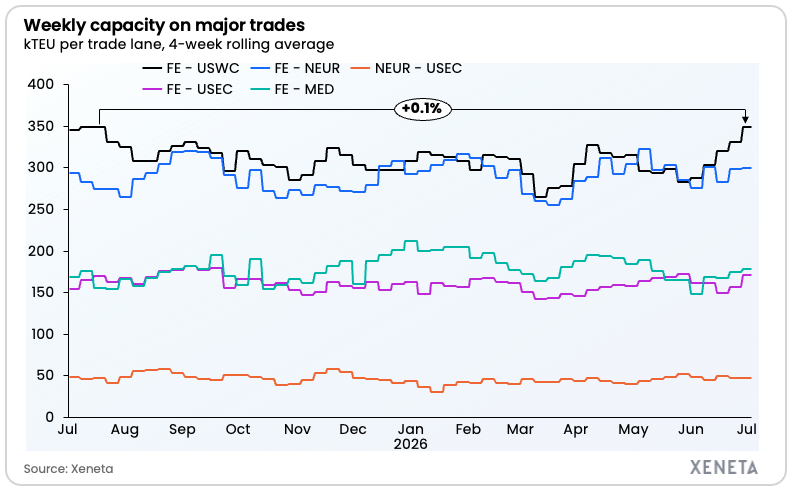

Offered capacity on major fronthaul trades (4-week rolling average) – w/c 29 June 2026:

-

Far East to US West Coast: +5.5% from a week ago

-

Far East to US East Coast: +9.0% from a week ago

-

Far East to North Europe: +0.4% from a week ago

-

Far East to Mediterranean: +1.7% from a week ago

-

North Europe to US East Coast: +0.2% from a week ago

Ends