The Xeneta Weekly Ocean Container Shipping Market Update provides data and intelligence including the latest freight rate and capacity movements across global trades with supporting insight from Peter Sand, Xeneta Chief Analyst.

Xeneta analyst insight - shippers face doubling freight rates and delays exporting goods out of Asia

Peter Sand, Xeneta Chief Analyst:

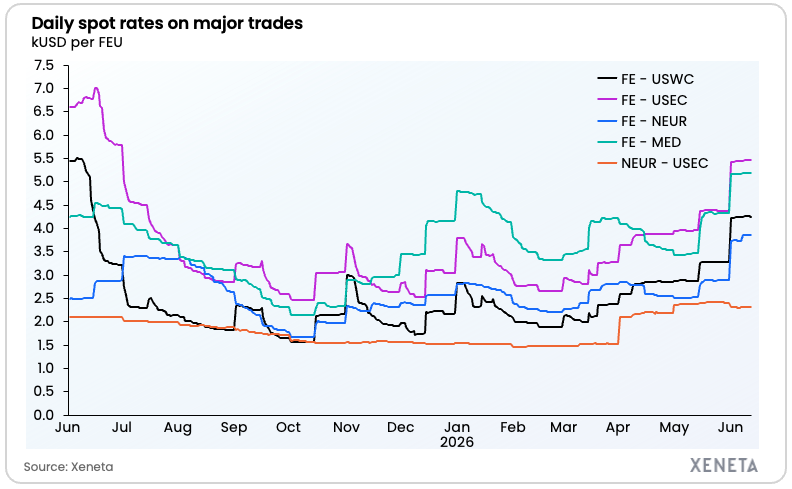

“Spot rates remain elevated across major fronthaul trades with further increases expected mid-June as disruption from Middle East conflict continues to bite hard. From Far East to US West Coast and US East Coast, spot rates are up 127% and 106% respectively since pre-Strait of Hormuz crisis and could double again before peaking. It is possible rates could get close to the Red Sea crisis peak in 2024, so shippers should act decisively to reduce their exposure to the spot market.

"Shippers are not only paying the price in freight rates, there are also delays exporting goods out of the Far East. Even large volume shippers with valid long term contracts are unable to move containers, with carriers stating services are fully booked into July. But a ship that is fully booked weeks into the future did not become fully booked yesterday – this demand has been building, so what have carriers been waiting for?

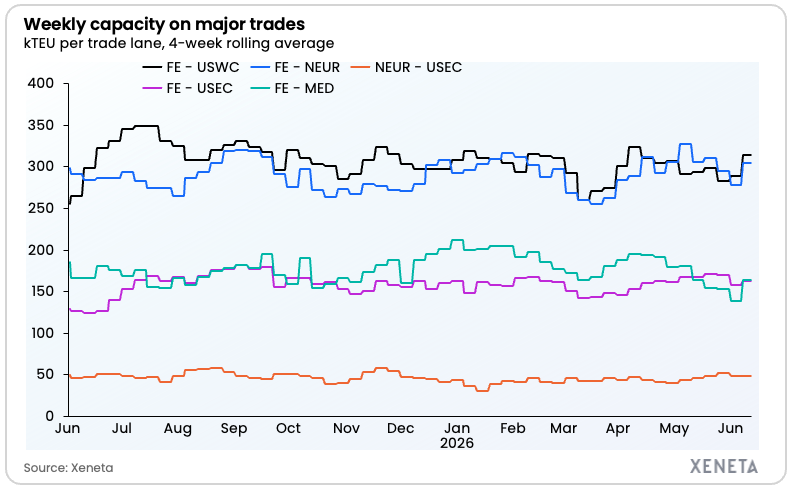

“Offered capacity on Far East fronthauls is essentially flat compared to pre-Strait of Hormuz crisis, up +1% to both US West Coast and US East Coast, up +2% into North Europe and down -7% into Mediterranean. Offered capacity is now starting to increase, but rates have already spiralled and containers are being rolled, so it is a case of too little, too late for shippers.

"Carriers driving up freight rates and rolling containers risks damaging relationships with shippers who remember how they are treated during the tough times. But carriers entered 2026 fearing a loss-making position, so they will do what they can to manage capacity and bank every dollar while they have the opportunity. Carriers may be fighting for the volumes of these same shippers when rates eventually soften and capacity loosens, but they will worry about that later.”

Data highlights

Market average spot rates – 12 June 2026

- Far East to US West Coast: USD 4 258 per FEU

- Far East to US East Coast: USD 5 462 per FEU

- Far East to North Europe: USD 3 854 per FEU

- Far East to Mediterranean: USD 5 194 per FEU

- North Europe to US East Coast: USD 2 315 per FEU

Spot rate changes since the end of February (pre-crisis) – 12 June vs 28 February 2026

- Far East to US West Coast: +127%

- Far East to US East Coast: +106%

- Far East to North Europe: +74%

- Far East to Mediterranean: +56%

- North Europe to US East Coast: +57%

Offered capacity on major fronthaul trades (4-week rolling average) – w/c 8 June 2026

- Far East to US West Coast: +8.7% from a week ago

- Far East to US East Coast: +3.3% from a week ago

- Far East to North Europe: +9.2% from a week ago

- Far East to Mediterranean: +18.1% from a week ago

- North Europe to US East Coast: +0.1% from a week ago

Offered capacity compared to pre-Strait of Hormuz crisis – 12 June vs 28 February 2026

- Far East to US West Coast: +1%

- Far East to US East Coast: +1%

- Far East to North Europe: +2%

- Far East to Mediterranean: −7%

- North Europe to US East Coast: +21%

Ends

Journalists can be added to the distribution list for Xeneta Weekly Market Updates by emailing press@xeneta.com.

Xeneta’s Media Contacts

Philip Hennessey

Director of External Communications, Xeneta

+44 7830 021808

press@xeneta.com