The Xeneta Weekly Ocean Container Shipping Market Update provides data and intelligence including the latest freight rate and capacity movements across global trades with supporting insight from Peter Sand, Xeneta Chief Analyst.

Xeneta analyst insight

Peter Sand, Xeneta Chief Analyst:

“It is still a very challenging market, but there is a faint glimmer of light at the end of the tunnel for shippers after spot rates remained essentially flat on major trades out of the Far East this week and carriers continue to increase offered capacity. This is by no means an end to the freight rate spike driven by the Strait of Hormuz crisis and further increases are expected mid-July, but these should be of a lower order of magnitude compared to the start of the month.

“Context matters because spot rates from Far East to US West Coast and US East Coast still sit +276% and +232% since the end of February. These are extraordinary levels and shippers are still paying multiples of what they were expecting to pay at the start of the year.

“What has changed is the supply side. Carriers have continued to deploy more capacity into the market – Far East to US West Coast is up 5.5% week on week, US East Coast up 6.2% and North Europe up 3.1%. That sustained capacity injection appears to be having an effect, easing some of the pressure and helping shippers to move goods more reliably, even if it is not yet translating into lower rates.

“We are at the beginning of the traditional peak season and the Strait of Hormuz remains effectively closed to container shipping. What we can say is that the market has paused for breath – and for shippers who have endured months of spiralling costs, that is at least a small piece of welcome news – for as long as it lasts.”

Data highlights

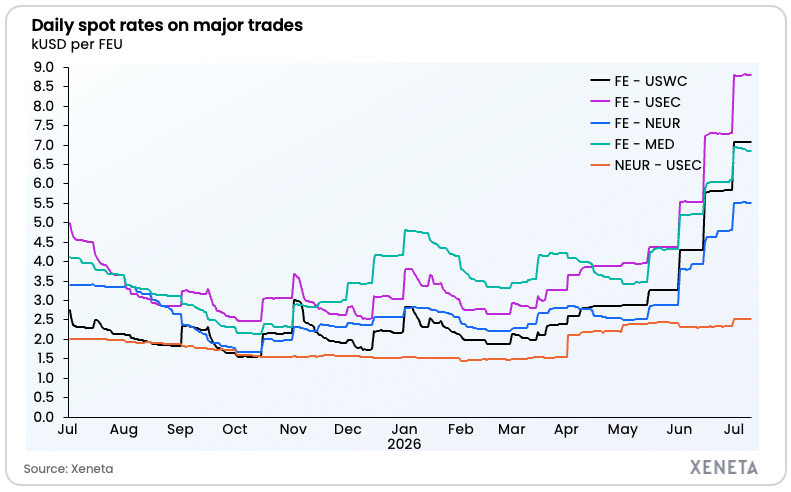

Market average spot rates – 10 July 2026

- Far East to US West Coast: USD 7 069 per FEU (40ft container)

- Far East to US East Coast: USD 8 808 per FEU

- Far East to North Europe: USD 5 503 per FEU

- Far East to Mediterranean: USD 6 855 per FEU

- North Europe to US East Coast: USD 2 531 per FEU

Spot rate changes over the past week – 10 July vs 3 July 2026

- Far East to US West Coast: -0.1%

- Far East to US East Coast: 0.3%

- Far East to North Europe: -0.2%

- Far East to Mediterranean: –0.9%

- North Europe to US East Coast: 0%

Spot rate changes since the end of February (pre-crisis) – 10 July vs 28 February 2026

- Far East to US West Coast: +276%

- Far East to US East Coast: +232%

- Far East to North Europe: +148%

- Far East to Mediterranean: +106%

- North Europe to US East Coast: +71%

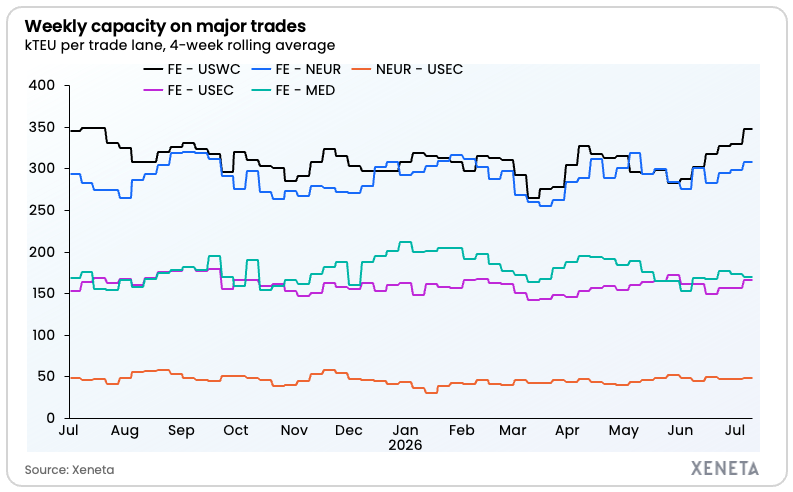

Offered capacity on major fronthaul trades (4-week rolling average) – w/c 6 July 2026

- Far East to US West Coast: +5.5% from a week ago

- Far East to US East Coast: +6.2% from a week ago

- Far East to North Europe: +3.1% from a week ago

- Far East to Mediterranean: –2.3% from a week ago

- North Europe to US East Coast: +3.8% from a week ago

Ends