The Xeneta Weekly Ocean Container Shipping Market Update provides data and intelligence including the latest freight rate and capacity movements across global trades with supporting insight from Peter Sand, Xeneta Chief Analyst.

Xeneta analyst insight - no hiding place for shippers with freight rates set to rise further in June

Peter Sand, Xeneta Chief Analyst:

“Early Xeneta data shows average spot rates on the Transpacific trade into US West Coast at the start of June are set to exceed +80% above pre-Middle East conflict levels. It is a similar story on fronthaul trades from the Far East to US East Coast, North Europe and Mediterranean which will see spot rate increases of +70%, +44% and +40% respectively compared to the end of February.

“It’s time to face reality - this crisis has gone on too long, the freight rate spikes are too severe and the geopolitical situation remains too volatile for shippers to recover the financial damage in the second half of the year. The question is what shippers do now to limit the full year impact on budgets which have once again been blown apart by geopolitical conflict.

“Those shippers who delayed locking into new long term contracts in the hope the spot market eases as new supply chain networks are set up in the Middle East cannot kick the can down the road forever. If they blink first and lock into a long term rate now, they could limit the damage in the second half of the year, even though they may be paying more than they budgeted for 2026. Continuing to play on the spot market could be costly given rates are still on an upward trajectory during a traditionally slack time of year.

“There is no hiding place from this market turmoil, with the latest June increases on the Transpacific driven mainly by the market mid-low, which are the rates generally paid by the larger volume shippers who command greater negotiating power. Carriers entered the year facing a potential market collapse as services return to the Red Sea, but have ultimately found themselves able to charge higher and higher rates to shippers across the market willing to pay a premium to protect supply chains against global uncertainty.”

Data highlights

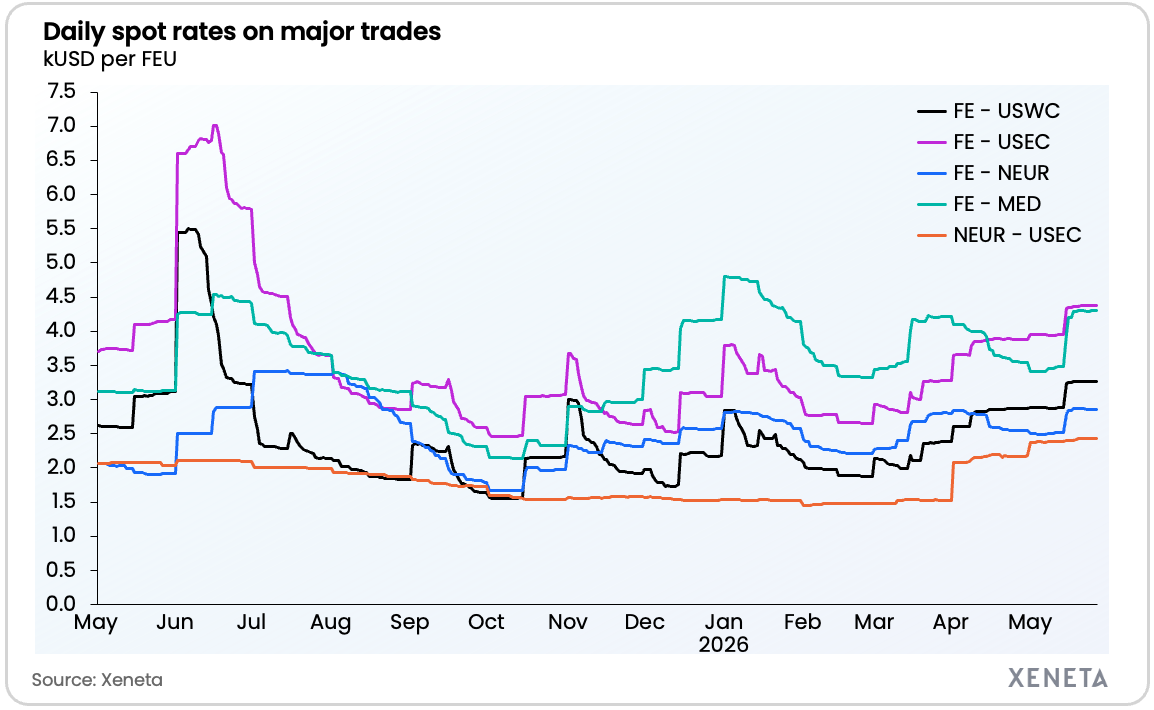

Market average spot rates – 27 May 2026

-

Far East to US West Coast: USD 3,272 per FEU (40ft container)

-

Far East to US East Coast: USD 4,372 per FEU

-

Far East to North Europe: USD 2,860 per FEU

-

Far East to Mediterranean: USD 4,304 per FEU

-

North Europe to US East Coast: USD 2,427 per FEU

Early Xeneta data for spot rates at the start of June compared to end of February (pre-crisis)

-

Far East to US West Coast: +80%

-

Far East to US East Coast: +70%

-

Far East to North Europe: +44%

-

Far East to Mediterranean: +40%

-

North Europe to US East Coast: +57%

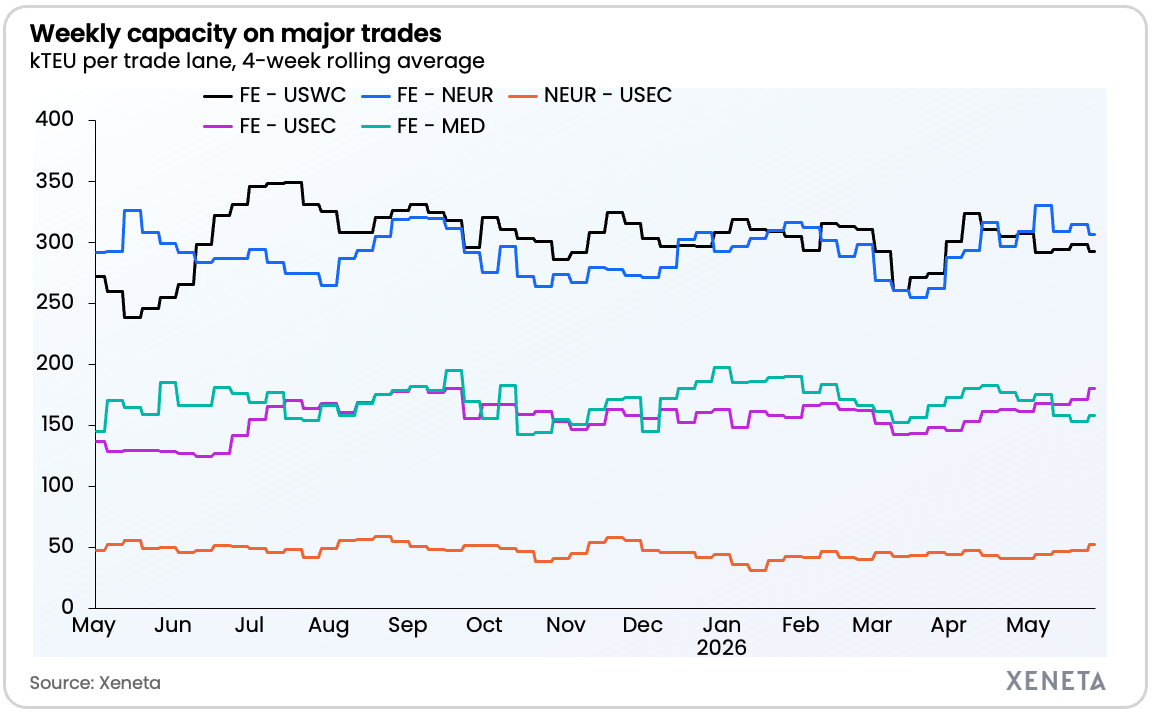

Offered capacity (4-week rolling average) – w/c 25 May 2026

-

Far East to US West Coast: -1.8% from a week ago

-

Far East to US East Coast: +5.5% from a week ago

-

Far East to North Europe: -2.5% from a week ago

-

Far East to Mediterranean: +3.4% from a week ago

-

North Europe to US East Coast: +10.4% from a week ago

Ends