.png?width=1200&name=straight-of-hormuz-imagery%20(1).png)

Ocean freight procurement has always required nerve. But this tender season is testing shippers in ways that feel uncomfortably familiar, and some ways that are entirely new.

The Middle East conflict has sent war risk premiums and bunker fuel surcharges surging, spot rates on directly-affected trades have spiked to around $4,000 per container into the Persian Gulf, and carriers are using market volatility as cover for pushing harder in early bid rounds. At the same time, the underlying freight market fundamentals (fleet overcapacity, slowing demand growth, carriers hungry for guaranteed volume) still favour shippers on most of the world's major trade lanes.

The key question for procurement and supply chain teams currently in negotiations: which signal do you follow? BCO (Beneficial Cargo Owner) contract data gives a clear answer. Shippers who stay disciplined, separate the noise from the fundamentals, and use the right levers at the right moments are landing rates significantly below the current long-term market average.

The market picture: volatility on top, oversupply underneath

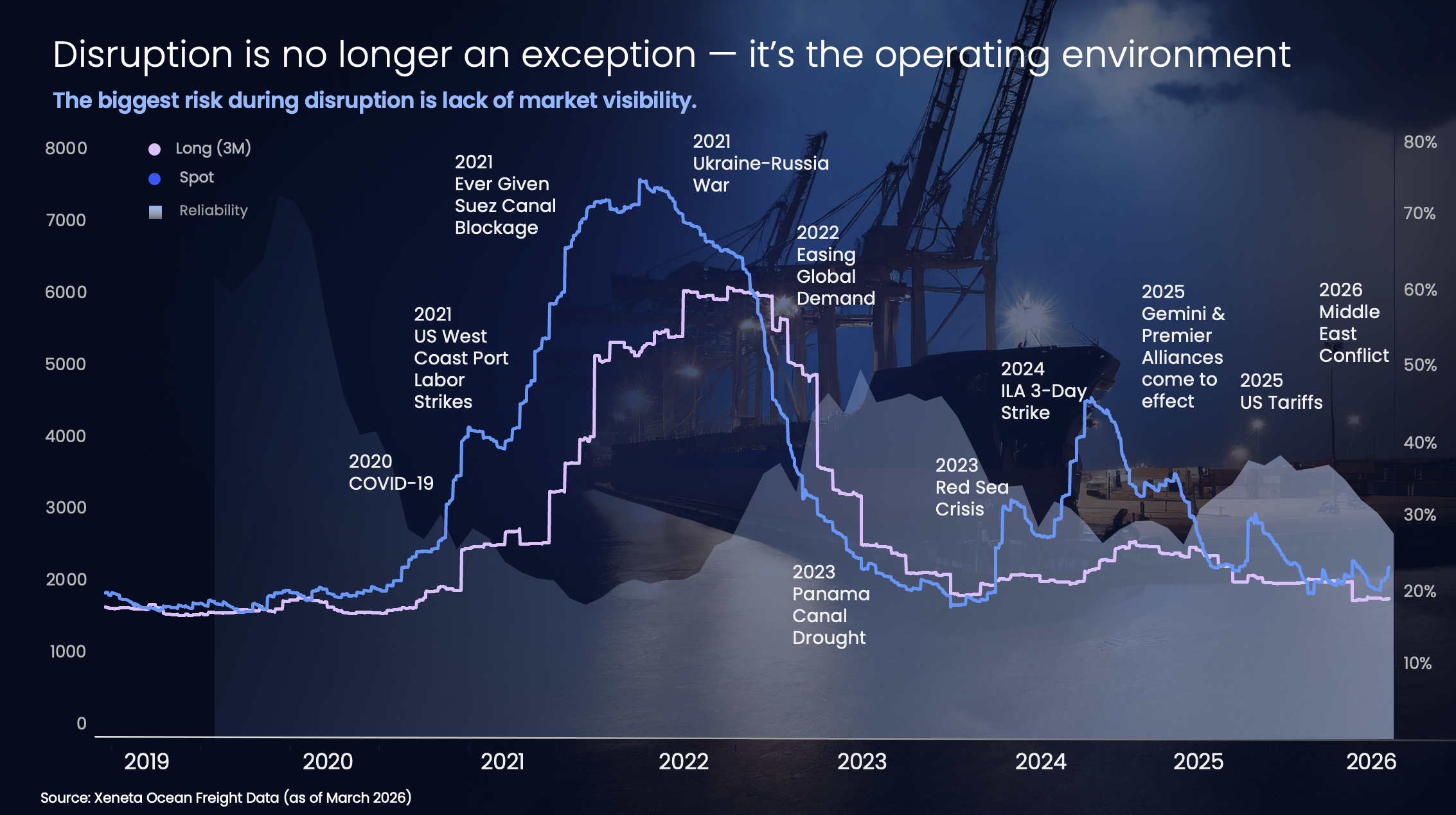

Container freight markets have an almost mechanical relationship with geopolitics. Rates spiked during COVID-19, fell sharply post-pandemic, surged again with the Red Sea crisis, and rose once more as the Middle East conflict deepened in early 2026.

That pattern also holds in reverse for service quality. Container shipping is arguably the only industry where higher prices correlate with worse customer service: Xeneta data shows that during COVID-19, on-time vessel reliability fell to around 20 percent as spot rates hit historic highs. Reliability dropped again with the Red Sea crisis and is falling again now.

On Far East to North Europe, spot rates climbed aggressively from late February before plateauing and falling back in mid-April. On the US trades, upward pressure has been more sustained, though softening is expected to follow within weeks. The top four trades (Far East to North Europe, Far East to Mediterranean, Far East to US West Coast, and Far East to US East Coast) are closely interconnected and movements on one typically propagate to the others.

Bunker fuel is the most immediate cost driver. Certain fuel types saw surcharge additions of over $1,000 per container in early March, and costs remain 40 to 50 percent above late February levels despite partial moderation.

The underlying fleet dynamic is keeping a floor under rates. Ships diverting around Africa rather than transiting the Red Sea cover significantly more distance per voyage, meaning the same number of vessels complete fewer round trips per year. That effectively removes capacity from the market and limits how far rates can fall. But it is not enough to reverse the overall trajectory. Fleet supply is growing faster than cargo demand, and demand growth forecasts are being revised down as the conflict, higher inflation, and slower GDP growth feed through. Carriers cannot fully pass fuel costs on, and that dynamic is showing up directly in tender data.

Should you delay your tender?

When the crisis broke in late February and early March, many shippers paused negotiations. The instinct to wait was understandable.

The data suggested that waiting was the wrong call for trades outside the Middle East. Carriers had adjusted to current conditions and still needed guaranteed volume. Shippers who continued negotiating through the disruption reported achieving rates well below the long-term market average, while those who paused found that the delay yielded little advantage and the window for this tender cycle continued to narrow.

Why Q2 remains the most popular time to tender

Contract timing matters as much as negotiation tactics. Based on BCO customer data, around 70% of long-term contracts commence between Q2 and Q3, with May alone accounting for 22% of all contract start dates. Part of this is structural, but part is simply habit: once a shipper has signed a 12-month contract, renewal comes around at the same time every year. Like a birthday, except with more spreadsheet admin and fewer celebrations.

The concentration in Q2 is not arbitrary. Three periods carry a structural disadvantage: summer peak season, when spot rates tick upward and carriers hold firmer; October to November, when carriers frequently call for end-of-year rate increases; and the Chinese New Year window, when short-term demand spikes compress carrier flexibility. The March to early June window, after CNY and before summer peak, gives shippers the most structural advantage. This year that window opened later than expected due to the conflict, but for most trades outside the Middle East it remains open now.

The Middle East exception

Shippers with freight moving directly into the Persian Gulf are operating in a different market entirely. Spot rates have reached approximately $8,000 per container, but the more significant problem is that ocean capacity has effectively collapsed.

A rate locked in at $8,000 today reflects a situation of near-zero capacity. When capacity does return, that rate will bear no relation to the market that re-emerges. A full Red Sea normalisation is not expected before 2027 at the earliest, with CMA currently testing a limited number of services but the broader return significantly delayed.

For Middle East-bound freight: use spot to move what must move, and delay long-term contract negotiations until capacity returns and the market settles.

Four things the best-performing shippers are doing differently

-

Separating surcharges from base rates. The biggest risk this season is paying both an emergency fuel surcharge now and a BAF (bunker adjustment factor) update three months later, effectively paying twice for the same cost event. Top performers are negotiating surcharges separately from the base rate and establishing explicit trigger mechanisms for when they apply and fall away. Rates with the fuel surcharge broken out are currently running approximately $200 per container higher on Far East to North Europe than all-in rates, with the surcharge itself averaging around $750. That looks more expensive today, but shippers with the surcharge separated have a mechanism to reduce total cost as bunker prices moderate. Shippers without that separation do not. Across trades outside the Middle East, fuel surcharges are negotiable, with BCO customers achieving around 50 percent reductions from initial carrier levels.

-

Using leverage late, not early. Unlike 2025, when the biggest improvements came between rounds one and two, this year carriers are holding firmer early and conceding at the final nomination stage when faced with credible volume reallocation risk. Shippers who contact their incumbent at the point of nominations, with a genuine best bid from a non-incumbent in hand, are seeing immediate rate realignment.

-

Engineering competitive tension. The best bids come from non-incumbent carriers willing to gain volume share. Top-performing shippers use those bids as active leverage against incumbents, and some are shifting allocations across lanes to make the threat credible. Competitive tension is engineered, not assumed.

-

Anchoring to forward-looking market data. Leading teams benchmark tender bids against data that reflects where rates are likely to be when the contract becomes valid, in three to six months, not where they are today. Anchoring to today's long-term rate, let alone last year's contract, means accepting a rate the market will likely move below before the ink is dry.

The case for indexation

For teams who want to go further than a fixed negotiated rate, contract indexation is gaining traction. Rather than fixing a price for 12 months, indexation builds in a mechanism that tracks the market throughout the contract period. There is also a growing shift toward shorter 3-6 month contracts as shippers look for more flexibility in volatile conditions. The goal in either case is not the lowest possible starting rate. It is making sure your containers ship, at a price close enough to market that carriers have no incentive to deprioritise your cargo when capacity tightens. Xeneta Academy's course on indexing and derivatives is a useful starting point for teams exploring this approach. For most shippers, getting containers moved reliably is the all-important outcome.

For a full walkthrough of the BCO tender data, including carrier-by-carrier bid movements from round one to round three, watch our on-demand webinar here or access the summary video.

To see how your current bids compare to the market and where the leverage sits on your specific lanes, explore Xeneta's freight intelligence platform.

.jpeg?width=387&name=AdobeStock_481214335%20(1).jpeg)