The Xeneta Weekly Ocean Container Shipping Market Update provides data and intelligence including the latest freight rate and capacity movements across global trades with supporting insight from Peter Sand, Xeneta Chief Analyst.

Xeneta analyst insight

Peter Sand, Xeneta Chief Analyst:

Elevated Transpacific ocean freight rates plateau:

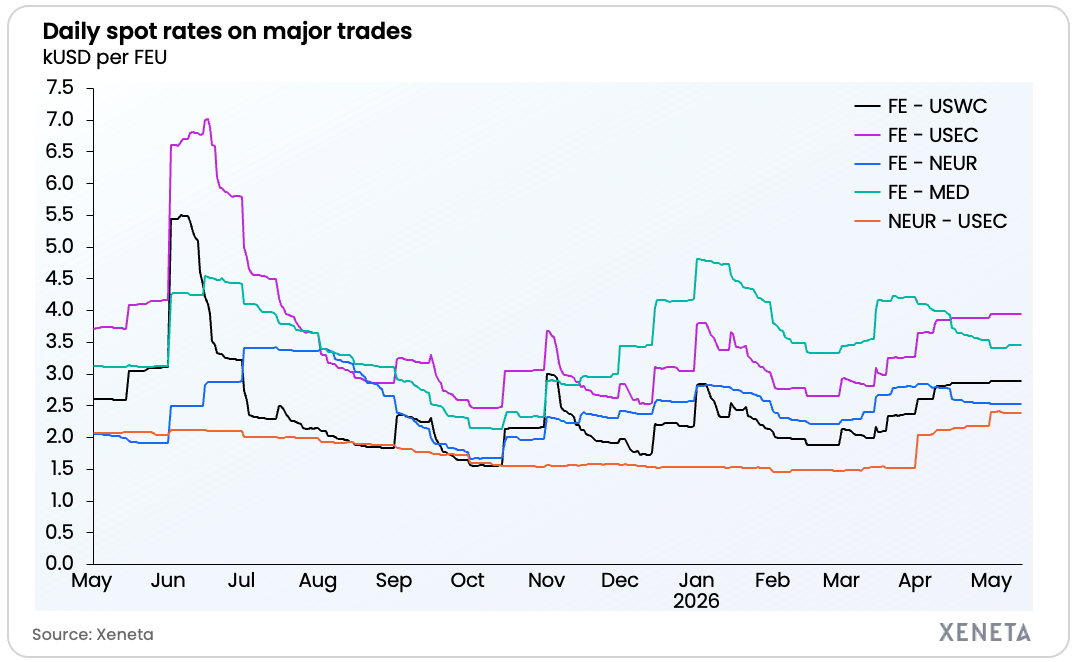

“Volatility in global ocean container supply chains means it is not often both shippers and carriers are ‘happy’ with the price they are buying and selling freight, but that is seemingly the case on Transpacific trades as average spot rates plateau at elevated levels amid ongoing conflict in the Middle East.

“Average spot rates from Far East to US West Coast remain up more than 50% compared to pre-conflict at the end of February, but have remained effectively flat over the past month.

“One factor behind the short term market plateau on the Transpacific is US shippers delaying signing new long term contracts due to the uncertainty caused by the Middle East crisis and the risk of locking in rates for the next 12 months at a higher level than necessary. For every delayed contract, more containers must be moved on the spot market and carriers will charge a premium – but for shippers, the short term pain is worth it if they ultimately secure lower long term rates in the coming weeks.

“This plateau will not last and volatility is never far away in ocean container shipping. Large shippers do not want to rely so heavily on the spot market and will be tempted into signing new long term contracts by carriers offering discounts to secure volumes for the next 12 months.

“As new long term contracts are finalised and come into force, volumes will shift back to contracted rates and that should translate into a softening of the short term market. This will be gradual softening rather than a dramatic fall off a cliff edge back to pre-conflict levels, particularly ahead of the traditional peak season build-up later in the summer.”

European spot rates falling back towards pre-Middle East conflict levels:

“The European-bound trades continue to tell a fundamentally different story. Far East to Mediterranean rates are now just 4% above pre-crisis levels – effectively back where they were before the Strait of Hormuz closed.

“What this demonstrates is that the carrier workarounds on these corridors – the land bridges, the rerouting, the new service networks built around the disrupted areas – are now functioning well enough that the market has largely absorbed the crisis as underlying overcapacity reasserts itself.

Data highlights

Market average spot rates – 13 May 2026

-

Far East to US West Coast: USD 2 884 per FEU (40ft container)

-

Far East to US East Coast: USD 3 974 per FEU

-

East to North Europe: USD 2 531 per FEU

-

Far East to Mediterranean: USD 3 451 per FEU

-

North Europe to US East Coast: USD 2 391 per FEU

Spot rate changes over the past month – 13 May vs 13 April 2026

-

Far East to US West Coast: +2% (USD 2 826 to USD 2 884 per FEU)

-

Far East to US East Coast: +2% (USD 3 858 to USD 3 974 per FEU)

-

Far East to North Europe: –8% (USD 2 763 to USD 2 531 per FEU)

-

Far East to Mediterranean: –12% (USD 3 929 to USD 3 451 per FEU)

-

North Europe to US East Coast: +13% (USD 2 124 to USD 2 391 per FEU)

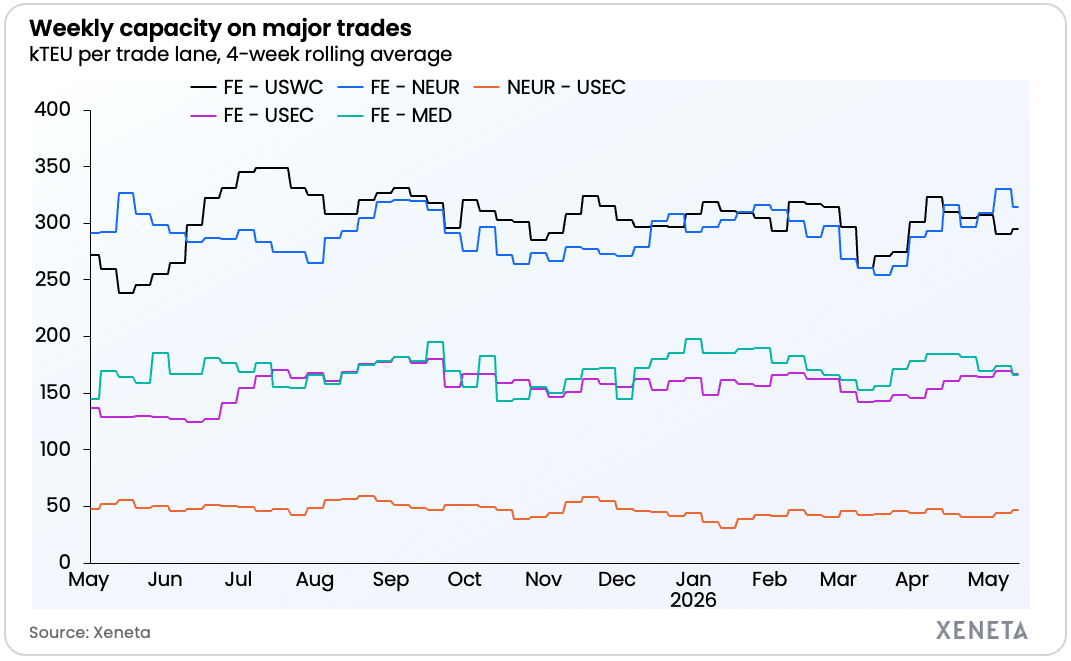

Offered capacity on major fronthaul trades (4-week rolling average) – w/c 11 May 2026

-

Far East to US West Coast: +1.6% from a week ago

-

Far East to US East Coast: −1.7% from a week ago

-

Far East to North Europe: −5.0% from a week ago

-

Far East to Mediterranean: −5.0% from a week ago

-

North Europe to US East Coast: +5.9% from a week ago

Ends

Journalists can be added to the distribution list for Xeneta Weekly Market Updates by emailing press@xeneta.com.