General Rate Increases (GRIs) have been a persistent talking point for the ocean freight sector since April this year, as carriers struggle to tackle a lop-sided supply-demand dynamic and elevate subdued rates. However, until now, those efforts have largely fallen flat. But have August’s GRIs succeeded in changing that narrative? Xeneta’s latest data appears encouraging for carriers…

2023 has seen the container shipping industry striving to overcome the ‘double whammy’ of declining volumes and escalating overcapacity, leading to lower rates and lost revenues. As such GRIs have been deployed in an attempt to jumpstart rates growth, but, looking at key Far East export corridors, have so far failed to make the desired, lasting impact.

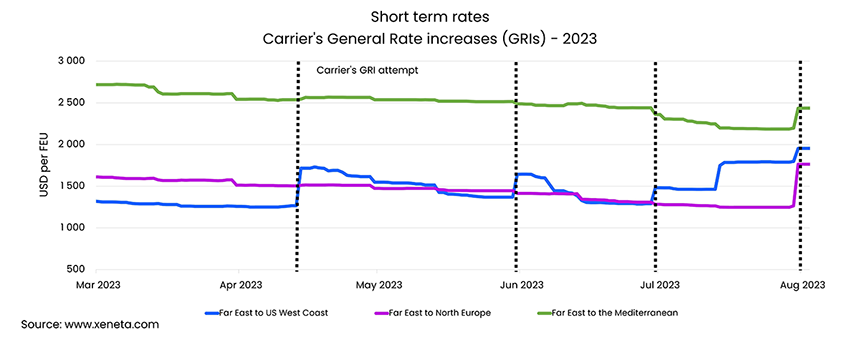

Getting a GRIp

The Far East to US West Coast route displays the clearest GRI influence from the months of May through to August. Here, since the end of June, trans-Pacific spot rates have climbed by 51.5% after three consecutive, and at least partially successful, GRI pushes.

For the Far East to North Europe trade lane, the spot rate fell below USD 1 500 per FEU in early May. However, from the end of July to the beginning of August, spot rates rose by 39.6%, an increase of USD 500.

This change has narrowed the spread between Far East to North Europe and Far East to the Mediterranean to just USD 670—the closest it’s been all year.

Limited success?

Looking at the bigger picture, the new GRIs have clearly had an impact, pushing the short-term market above the long-term on all three leading corridors. So, have they been “successful”? In July, many of the key carriers suggested they were looking to raise rates by USD 1000 per FEU and, by this measure, the GRIs have fallen short.

According to Xeneta data, the market average spot rate per FEU from the Far East to the US West Coast increased by USD 470 from 1 July - 1 August, remaining in that range this week. This is the largest climb across the earmarked corridors and is, clearly, far below the targeted increase. However, given the lackluster trajectory of rates up until this point, the hikes will no doubt be welcomed within the carrier community.

Too soon to tell

With the traditional peak season for container shipping now looming large, shippers who have been taking advantage of the subdued spot market may wonder if they have left it “too late” to sign new long-term contracts. However, given that the market has shown significant weakness upon implementation of GRIs earlier in the year, it is still too soon to know if the hikes are here to stay, and how the next round of GRIs (in September) will fare.

Stay tuned for the latest developments, analysis and negotiating intelligence in the ever-evolving rates marketplace.

Want to learn more?

Contact us to learn how Xeneta can help you prepare for this upcoming tender season and supplier/buyer negotiations. Gain the upper hand with actionable real-time ocean and air freight rate and capacity data.