.avif)

Welcome to the Xeneta monthly schedule reliability update, where we review what the latest reliability developments are signaling across the global supply chain – and what to carry forward into next month’s operations.

Global

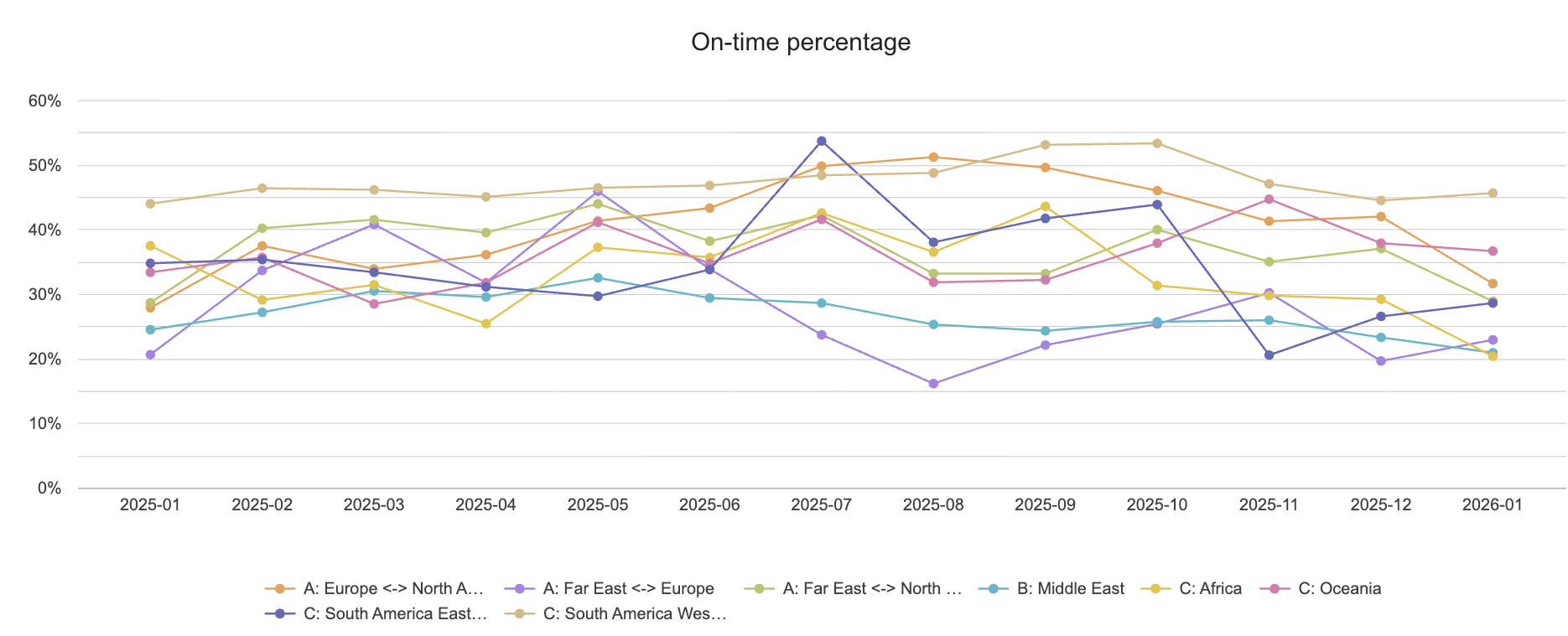

The mid-2025 ceiling of 38% gave way to uncertainty in Q4 and the start of 2026 shows us this slide was not an exception.

Global Monthly On-Time Arrivals by Trade, 2025 - 2026

Global on-time performance in January has continued to decline, landing at 29% of arrivals on-time. This marks a departure from the characteristic sideways progression of 34-37% of monthly on-time arrivals that we observed in Q2 and Q3 in 2025. Compounding the decline is the magnitude of delays, from 3.7 days up to 4.2 days at berth arrival. This means that we didn’t just see more late arrivals, but also an increase in the severity of those delays.

With tender season approaching fast, a consistent month-over-month decline from 37% in October down to 29% in January warrants scrutiny from shippers. Careful consideration of carrier-level performance balanced across transit times, on-time arrivals, and cancellation rates should be incorporated before firming contracts.

Trade

Trade reliability, as always, is a finer tuned indicator of where challenges to our supply chains lie and which geopolitical events are proving to be the most impactful.

This month the sharpest declines appeared on the following trades:

- Africa down by 9 points to 20% on-time

- Europe – North America down by 10 points to 32% on-time

- Far East – North America down by 8 points to 29% on-time

West Africa has seen consistent commercial growth by way of the Red Sea rerouting since Q1 2024, but many ports have remained hard-pressed to meet this with an equally accelerated improvement in infrastructure. The port of Conakry is a prime example, reportedly experiencing a 42% surge in activity in Q4 2025, with weekly average congestion topping 75% for the past 7 months.

The ongoing Red Sea uncertainty remains a major amplifier for the Africa trade, and this makes it a key market to watch for dynamic capacity shifts and swells of poor reliability in the event of a large-scale return to Suez Canal.

As for historically stable Europe – North America, much of the latest troubles on the transatlantic can be attributed to a series of severe weather disruptions. Repeat storms led some ports to announce several days of closure and racked up over a week of additional delays on multiple vessels to the East Coast North America across 16+ services. See our detailed coverage here.

The transpacific trade is currently seeing its worst reliability since January 2025, when the alliance turnover period brought it down to 29% of on-time arrivals. This year’s drivers are less dependent on dramatic network overhauls, but comparable in operational impact. Paired with the seasonal spike in cancellation rates in February and March totaling 687,000 TEU and 93 cancelled sailings, these delays indicate a rough start to 2026 for US shippers.

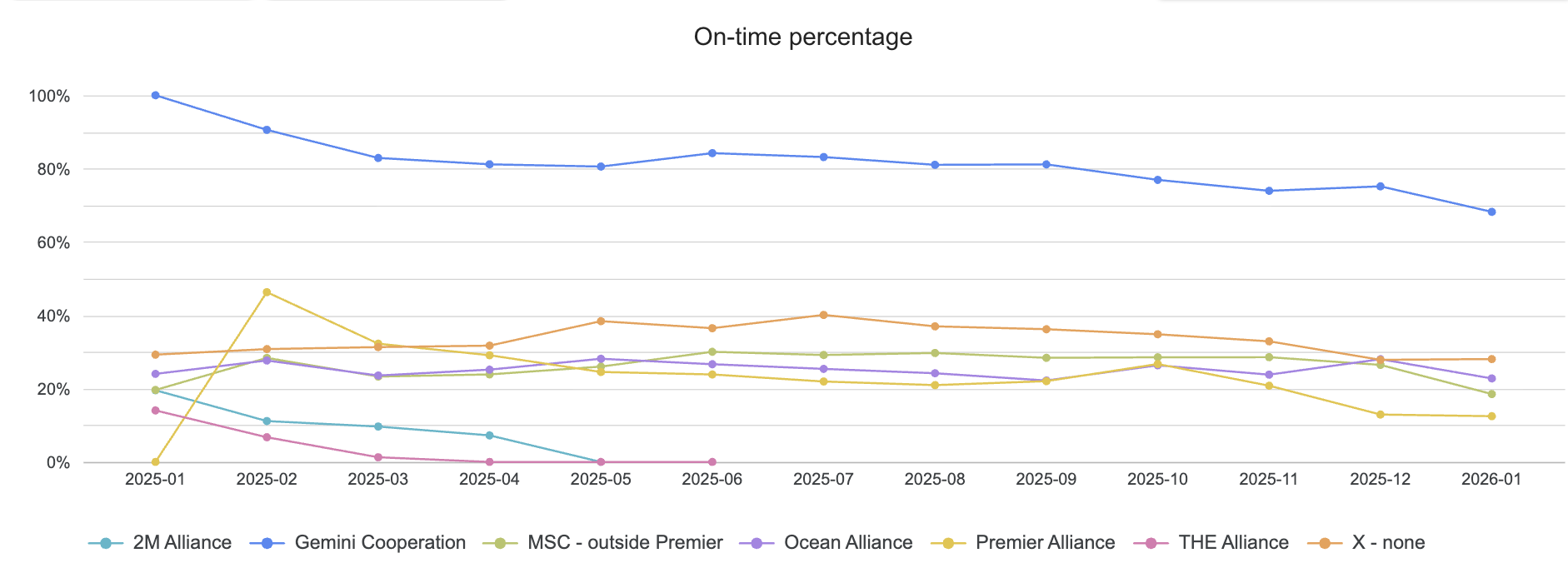

Alliances

The alliance hierarchy was largely unchanged in January within the scope of global reliability, but there was one modest outlier. Non-alliance strings remained stable at 28% of on-time arrivals and inched back into second place just ahead of Ocean Alliance, which fell by 5 points.

- Gemini Cooperation: 68% on-time

- Non-alliance: 28% on-time

- Ocean Alliance: 23% on-time

- MSC (outside Premier: 19% on-time

- Premier Alliance: 12% on-time

All networks with the exception of non-alliance services declined at the outset of 2026, highlighting the operational headwinds we can expect to face in Q1 and Q2. Ocean Alliance, MSC, and even Gemini all took considerable hits to their performance this past month, from 5 to 7 points of decline.

This concentration of negative impact tracks well with our trade level observations. MSC and Gemini, which each fell by 7 points, are both key players on the transpacific and transatlantic trades in terms of market share.

Volatile reliability patterns are fairly expected for MSC, but seeing the Gemini Cooperation lose some foothold lends a different weight to the severity of the localized issues. The dual pressure of prolonged wait times and congestion at Asian hubs throughout January, as well as widespread weather disruptions in the North Atlantic Ocean caused created operational strain for the most resilient network.

What’s next?

- We’re keeping our eyes on Premier Alliance’s promises of better network reliability with their 2026 Product promise. Read our thoughts on whether route optimization will be enough.

- Will the post-Lunar New Year period lead to a capacity surge in March, or will a soft market lead to aggressive tightening of capacity and increased cancellation rates? An overabundance of capacity on a trade like Far East – Europe can complicate recovery from embedded delays.

- The current reliability slump on what was a relatively resilient Far East – North America throughout 2025 will be one to watch. With tender season practically upon us, this is crucial for window shippers and forwarders to reexamine performance at a carrier level. For a breakdown of carrier-level performance on your port pairs, reach out to us today.

- Red Sea transits remain at the forefront of everyone’s minds and spell major shifts in reliability and capacity that extend beyond the Far East – Europe trade.

- Follow the latest insights and updates on our Red Sea News Hub.

.jpg?width=387&name=ocean-freight-shipping-reliability-scorecard--feb-26%20(1).jpg)