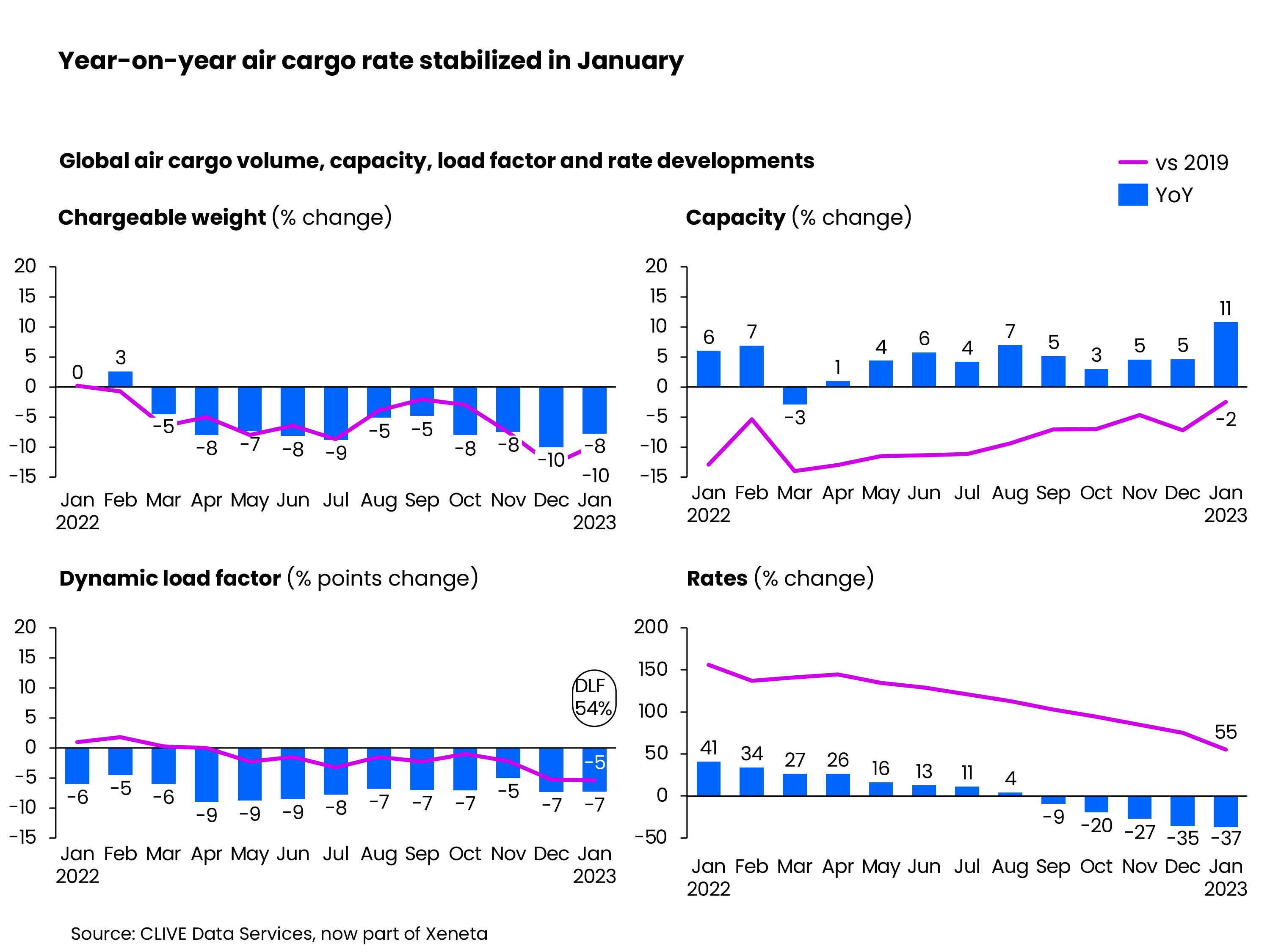

January was a dramatic month for long-term ocean freight rates, as rates dropped by 13.3%, according to the latest data from the Xeneta Shipping Index (XSI®). Global air cargo demand also continued to fall (-8%) due to an early Chinese New year this year and ongoing global economic troubles.

With the unpredictable global events currently creating havoc on the supply chains, learn what Xeneta experts have to say about the future of the ocean and air freight market.

The great turnaround in shipping | NPR

From charging ten-fold rates to struggling with overcapacity, carriers certainly are living the results of their rash decisions since the pandemic. But will the consumers see the benefits of the cost cuts and lower prices of goods?

Emily Stausbøll, market analyst at Xeneta, suggests consumers should not hold their breath for lower prices as carriers are doing everything they can to keep freight rates up.

Listen to the full conversation with NPR, where she talks about the great turnaround in shipping.

A wave of new container ships may help ease inflation sting | Bloomberg

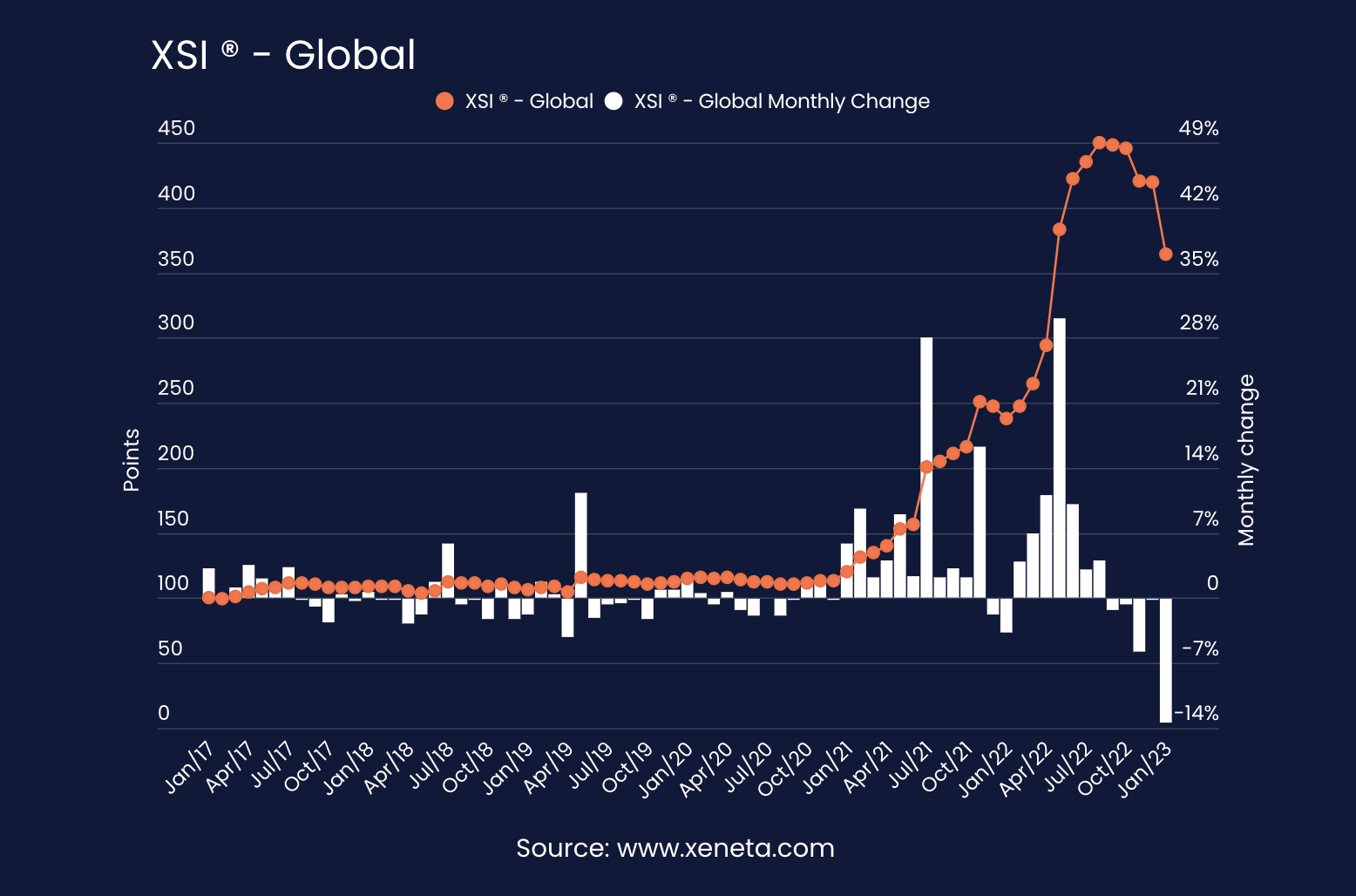

It’s not only spot container rates that are reflecting a supply-demand balance that’s shifted away from the shortages present just a year ago. The Xeneta Shipping Index for January showed a record-large drop in long-term rates — a month-over-month decline of 13.3%. Heading into contract negotiating season, that’s welcome news for the owners of cargo and others who’ve felt the sting of inflation stemming from soaring freight rates.

“Shippers, well aware of market dynamics turning in their favor, have reacted, pushing carriers for major rates reductions,” Xeneta CEO Patrik Berglund says in a press release Tuesday. “What we’re seeing now is the effect of that, as new contracts enter validity. And, for the carriers, worse is set to come.”

Xeneta green scheme names and shames box line heroes and villains | The Loadstar

Xeneta has bravely launched a “Heroes and Villains” campaign to ’name-and-shame’ the best and worst environmentally efficient carriers – starting with Hamburg Süd and Evergreen. Its findings highlight Evergreen as the worst performer among the top six carriers operating this trade, with a CEI measure of 109.7.

This compares with the overall ‘hero’ of the trade lane, Hamburg Süd – soon to be rebranded and absorbed into Maersk – which scored 76.2.

Lag effect: Why liner profits stay high much longer than spot rates | FreightWaves

Whereas the global WCI and FBX spot rate indexes peaked in September 2021, Xeneta’s XSI® long-term index didn’t peak until 11 months later, in August 2022.

The XSI® fell moderately in the fourth quarter, then registered its largest-ever month-on-month plunge — 13% — in January. Even so, the XSI® was still at 364 points last month, 3.4 times higher than the 2017-19 average. Read more.

Good times still rollin’ for shipping lines in trans-Atlantic trade | Freight Waves

Xeneta's short-term index put North Europe-U.S. East Coast rates at $6,086 per FEU as of Wednesday. Long-term rates for this trade were under $6,000 per FEU as of mid-January.

Spot rates have fallen below contract rates in almost all of the world’s container trades — but not yet in the trans-Atlantic westbound lane. In markets where spot rates have sunk well below contract prices, carriers have agreed to lower some of their long-term rates in mid-contract, further reducing revenues. That renegotiation dynamic does not apply in the trans-Atlantic.

Europe-U.S. rates remain “historically strong,” said Xeneta Chief Analyst Peter Sand earlier this month, adding that both short-term and contract rates in January 2021 “were roughly a third of today’s prices.”

Carriers face ‘horrific times’ after record fall in long-term rates | TradeWinds

Long-term container freight rates are falling at a record pace as contracts are renewed at lower levels. And worse could be in store as more contracts are set to expire in the coming months. Average long-term contracted rates dropped by 13.3% in January, their largest ever month-on-month drop, according to the Xeneta Shipping Index.

It is the fifth month in a row of falling prices, with little sign of change ahead in what looks like a challenging year for carriers. Read more.

Maritime logistics unplugged | Splash247

So long are the days when manufacturers were involved in distributing their products (1PLs). Instead, the market promoted the emergence of 2PLs and 3PLs, which became further integrated (4PLs and 5PLs) as their control over manufacturers’ activities increased to increase their power along the different chains in which they participate. Such integration, while resulting in a greater responsibility over supply chain activities, also contributes to obtaining a higher bargaining power, for instance, with ocean carriers when negotiating their contracts of carriage of goods, particularly in market conditions in which overcapacity dominates and there are no bottlenecks to absorb capacity as witnessed during the covid pandemic.

This intermediary’s negotiating power is well demonstrated by the different shipping indexes, particularly those related to container shipping, and confirmed by Emily Stausbøll, market analyst at Xeneta when claiming that shipping companies struggled to get freight rates up above their break-even levels during the decades pre-covid.

Read the full story by Ana Casaca, the CEO of World of Shipping Portugal, here.

Maersk warns global box volumes could slide 2.5% this year | Splash247

While much has been written about the declining spot rate environment, there is also now a record-breaking fall in long-term rates, according to Xeneta, a freight rate benchmarking platform. Average long-term contracted rates dropped by 13.3% in January, Xeneta reported last week.

Xeneta CEO Patrik Berglund commented: “Global demand has fallen away, congestion has eased, equipment is available, and the macro-economic and geopolitical situations are, to say the least, complex.” Read more.

Liners now in the red on a mark-to-market basis | Splash247

While much has been written about the declining spot rate environment, there is also now a record-breaking fall in long-term rates, according to Xeneta, a freight rate benchmarking platform. Average long-term contracted rates dropped by 13.3% in January, Xeneta reported this week.

Xeneta CEO Patrik Berglund commented: “Global demand has fallen away, congestion has eased, equipment is available, and the macro-economic and geopolitical situations are, to say the least, complex.” Read more.

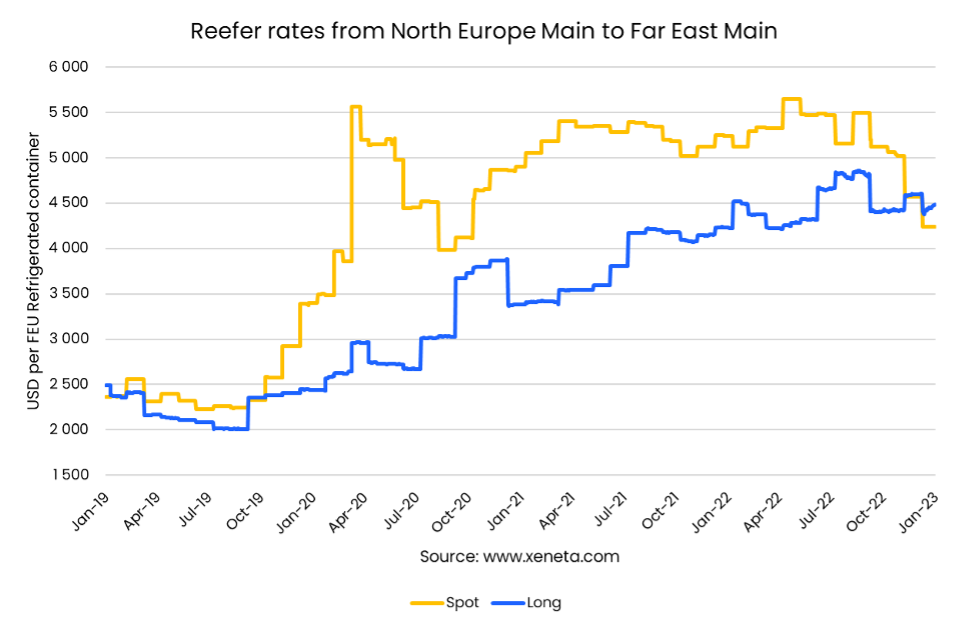

Cold reception for reefers in China sees volumes, and rates, slip on main Europe to Far East trade | Hellenic Shipping News

According to the latest data from Oslo’s Xeneta, the spot rate on the leading fronthaul reefer route now sits at USD 4 240 per FEU (23 January 2023). After a period of almost two years defined by prices in excess of USD 5 000 per FEU reefer container, a sharp fall in December has changed the character of the market, with spot rates now below-contracted prices for the first time since October 2019.

Xeneta’s crowd-sourced data shows a current long-term rate just shy of USD 4 500 per FEU reefer after peaking in September last year at USD 4 850.

“Spot rates falling below long-term contracts is a classic sign of a weak market,” comments Peter Sand, Chief Analyst, Xeneta. “This is one of the world’s busiest reefer routes, with a strong rates track record, but even it is not impervious to the forces impacting containerized freight at present.

CLIVE points to continued uncertainty in the air cargo market | Air Cargo News

The global average dynamic load factor, which Xeneta-owned CLIVE uses to measure cargo load factors by considering both the volume and weight perspectives of cargo flown and capacity available, reached 54% in the first month of this year.

Because of the airfreight industry’s capacity increase but volume decrease, the load factor fell by 7 percentage points. Compared to 2019, it was down by 5 percentage points as the demand/supply balance started to lean towards oversupply.

“The early Chinese New Year might be causing some noise in the January air cargo data with factories there closing ahead of the New Year, contributing further to a weak global market producing load factors at a level we haven’t seen for some time,” commented Niall van de Wouw, chief airfreight officer at Xeneta.

“So, there is still a high level of uncertainty, but if rates haven’t yet reached the 2019 level in value in the current climate, and with an expectation that inventory levels will need restocking at the end of Q2 and Q3, then it’s unlikely we will see spot rates return to the pre-pandemic level unless this happens soon. But this, of course, partly depends on consumers spending in a similar fashion as we have seen recently,” he added.

Want to learn more?

Sign up today for our upcoming monthly State of the Market Webinar to stay on top of the latest market developments and learn how changing market conditions might affect your contract negotiations.

Missed the LIVE session? Sign up to get the full webinar recording.