During one of the featured sessions at the sixth annual Xeneta Summit, Mark Szakonyi, Executive Editor at JOC, S&P Global Market Intelligence, and Peter Sand, Chief Analyst at Xeneta, shared what shippers will need to deal with container shipping challenges in 2023.

State of the Market

The start of 2023 has seen spot market rate reductions slow down significantly. This is mostly related to carriers removing capacity through blanked sailings and canceling services. The high level of blank sailings ahead of the 2023 Chinese New year showed just how low demand is, with little to prop carriers' hopes up for the rest of the year.

Despite a reduction in the spread between spot and long-term rates, many freight forwarders continue to shy away from the long-term market, preferring to move named account contracts (NACs) onto the spot market. This trend can be seen on many trades.

Using the Far East to North Europe trade as an example, Xeneta data (from the week of Jan 13, 2023) shows that only a couple of freight forwarders have managed to secure long-term rates lower than what is currently offered on the spot market.

Shaping the next decade

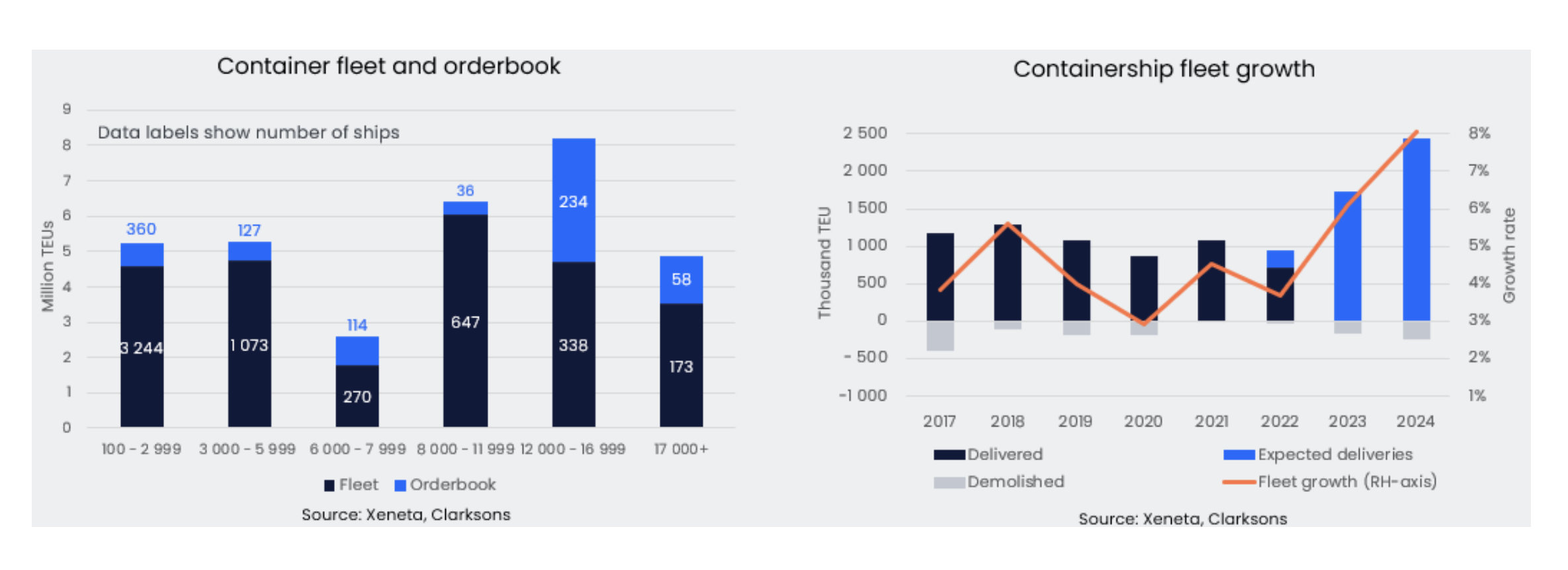

2023 will be all about increased injections of capacity, with most of that coming in the second half of the year. If we look at the percentage of the fleet on order, we can see the scale of new capacity joining what's already on the water.

There’s a lot of speculation about the impact of new IMO rules on ship design and energy efficiency in 2023. Mark points out that although the data will be collected from this year onwards, the enforcement and the real snapback on potential capacity will not come for at least another year.

Peter Sand highlights the seven million TEUs on order for delivery (as per data shared during Xeneta Summit in November 2022). Capacity will escalate for every quarter until mid-2024 and make 2025 another significant year. The next three years will be about managing the supply side for the carriers, while shippers and freight forwarders will be spoiled for choice.

Capacity management may not only be a game of blanking sailings. A million TEUs might get thrown into idle fleets in 2023 due to the huge gap in supply and demand.

But who is ordering this capacity?

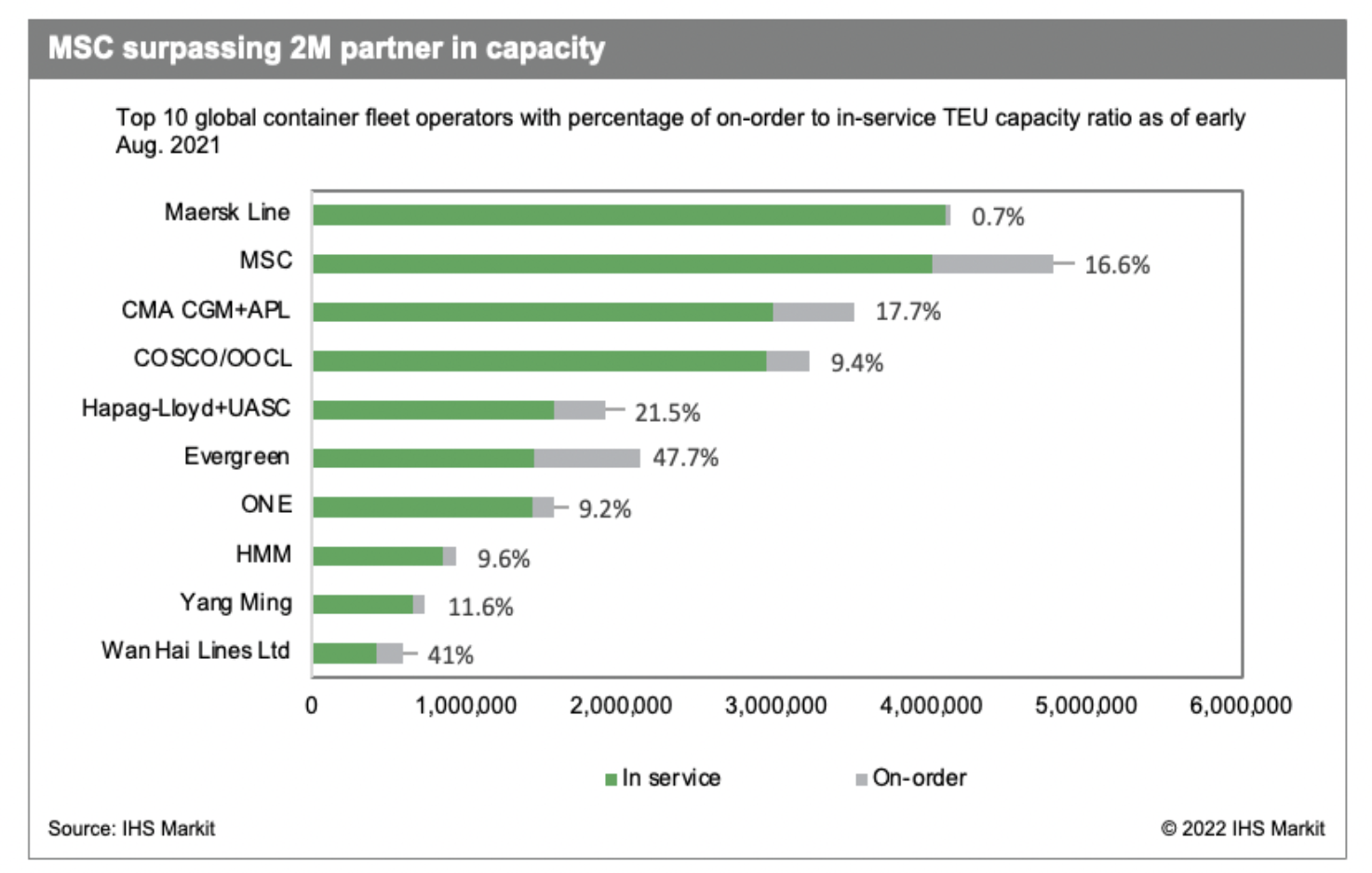

MSC's global deployed capacity had already surpassed Maersk's numbers as per August 2022 data from S&P Global. At the 2022 Xeneta Summit, Mark Szakonyi, Executive Editor at JOC, S&P Global Market Intelligence, discussed the future of the 2M Alliance as the mismatched capacity between the two alliance companies highlighted two very different directions.

And it seems he was right — in the week of Jan 23, Maersk and Mediterranean Shipping Company, the two largest lines in the world by active fleet capacity, announced an end to their 2M alliance.

Mark pointed out that an alternative arrangement will partly reflect the three or four-year integrator journey for these two companies as they try to connect all the pieces and provide better control of their assets.

A decade full of focus on emissions

A solution for decarbonizing the container shipping fleet will be another important factor to look out for in 2023 and the rest of the decade.

Buying sustainable fuel might solve all our problems, but the question is, what is the most preferred sustainable fuel of the future? Peter says shippers are the only part of the container shipping industry or global transport logistics chain that can support the green agenda as consumers.

That is why Xeneta launched its Carbon Emissions Index (CEI) in November 2022 in partnership with Marine Benchmark. A first-of-its-kind data solution, CEI shows the carbon intensity of the world's leading carriers across 13 main global trade lanes based on actual cargo load from real sailings.

Such solutions will also help in breaking the current industry dilemma regarding who should make the first move. Mark described this as a chicken-and-egg problem for the future of sustainable fuels.

Alliances are also feeling regulatory pressures. But it is yet to be seen how the greenhouse gas emission targets and the IMO 2023 will impact the capacity.

Peter says it will be difficult to single out the effect of regulations from the entire market development. It may be insignificant in the end because of other major factors also going in the same direction.

He believes that even if carriers claim that the new regulations will create an inefficient network, consuming an unimaginable amount of capacity, it will not be enough to stop the tsunami facing the market imbalance in the coming years.

Geopolitics will increasingly affect supply chains

The fact that the sale of a 24.9% stake in German terminals was debated in Berlin and was basically pushed or pulled through by Chancellor Scholz shows that geopolitics will affect global supply chains going forward. Peter warns shippers to prepare for the worst.

Another theme that has been all the hype in 2022 and 2023 is reshoring or nearshoring. A quick audience survey at Xeneta Summit revealed that none of our customers seriously considered reshoring or nearshoring before 2022, or plan to make major changes in the next few years.

Mark also highlighted that if we look at the data for US imports from Asia, even though the share from China has been a little bit static with certain categories (such as apparel) migrating into Vietnam and other places, the powerhouse remains China.

Xeneta experts believe we need multiple years of double-digit growth for containers out of Vietnam, for example, to be one of the key beneficiaries of the trade war between the US and China before we can see any major shift out of China.

The pandemic has done two things in terms of labor. It has increased the cost of living, putting pressure on labor to seek more work, but it has also shown labor's invaluable role in the supply chain. There has been an awakening of labor's power, and we might see its impact in the next couple of years.

Hopefully, Covid won’t be an issue for the supply chain in the next few years, but Xeneta analysts see many other global disruptions that might affect the markets.

The reopening of China and signs that inflation has peaked in many Western countries would normally point to volume improvements. However, with high inflation rates and Covid spreading in China, a flat or further fall in demand this year is still the most likely outcome.

Also, how carriers manage capacity will be crucial for rates. Will they continue to offer spot rates below their breakeven to secure volumes, or will even more capacity be taken out of service, either through idling or demolition?

Regulatory questions may put a limit on how much capacity is removed. However, as per a recent customer report from Xeneta, carriers have the reserves to idle ships if that is the alternative to an all-out price war.

Want to learn more?

Watch the latest monthly State of the Market Webinar to stay on top of the latest market developments and learn how changing market conditions might affect your contract negotiations.