-1.jpg)

Welcome to the June 2021 edition of the Xeneta Shipping Index (XSI®) for the long-term contract container market. As we ended the 1st half of a tremulous 2021, the global XSI ® went up by a further 2.3% in June-21 to 156.41 points.

Contract market rates now stand a staggering 39.2% up year-on-year (having risen 37.7% in 2021 alone). There appears to be little relief on the horizon for a financially battered shipper community.

“It can almost be difficult to keep a sense of perspective here,” comments Xeneta CEO Patrik Berglund. “Seen in the context of 2021, a 2.3% gain appears only moderate, but in any other month, in any other year, this is a very strong performance for the carriers.

And, he notes, there’s little relief in sight. Carriers are making bold moves to increase their fleets, but, for the most part, these are long-term decisions rather than short-term capacity injections. For example, HMM has just announced the ordering of twelve 13,000 TEU vessels, for $1.57bn, which will take the capacity of the Korean line past 1m slots, while Hapag-Lloyd has ordered six 23,500 TEU ships, with delivery expected from 2024.

In the meantime, the supply chain is buckling under the pressure. As Berglund explains: “Ports in the US are facing new levels of congestion, causing huge delays in shipments and inventory shortages for retailers. In fact, a recent survey by the National Retail Federation (NRF) found that 97% of members had been impacted by port and shipping delays, while President Biden has announced the creation of a Supply Chain Disruptions Task Force. And, looking further afield, let’s not forget Yantian and Shenzhen, which were hit by COVID a couple of weeks ago making it even more difficult to balance supply and demand.”

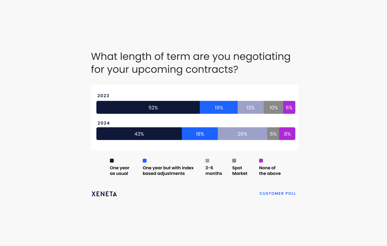

Short & Contract Market Delta Grows

Shippers are left with the unpalatable – some would argue unsustainable – combination of deteriorating reliability and climbing spot and contract rates. It’s exceptionally tough for shippers to navigate the market right now, as the delta between short and contract rates continues to grow. Carriers unquestionably have the upper hand and are in a strong position to exploit the budgets of big volume shippers.

“We should all brace ourselves for the carriers’ and forwarders’ Q2 financials. It will be a joyful moment for the sellers, but painful for the rest of the market. However, it’s universally positive that it gives the seller community an opportunity to invest those gains in more sustainable, eco-friendly infrastructure. We hope they seize it,” concludes Berglund.

XSI® - US Imports / Exports

US imports on the XSI ® jumped by 9.3% in June to 166.16 points. The month-on-month increase was the third largest on record and resulted in the benchmark being 36.9% higher than in Jun-20. The index has also now risen by 36.0% since the end of 2020. US exports continue to stutter and fell by 2.0% in June to 94.62 points.

[Blog post continues after banner.]

XSI® - Europe Imports / Exports

European imports on the XSI ® declined for the first time in seven months in June after the benchmark fell by 4.2% to 163.62 points. Despite the month-on-month decline, the index is still up 48.1% compared to the equivalent period of 2020 and has risen by 47.1% since Dec-20. More positively, exports continued to increase, jumping by a further 1.9% to 142.88.

XSI® - Far East Imports / Exports

Far East imports on the XSI ® rose by 1.5% to 134.41 points. While the index increased in June, the rate of growth was much lower than the jump of 13.8% recorded in the previous month. Nevertheless, the benchmark is up 27.3% year-on-year and has increased by 39.4% since the end of 2020. Exports also increased in Jun-21 rising by a further 2.0% to 201.54.

.