With the annual 2018 TPM conference in Long Beach having been and gone, Xeneta looks back at rate developments on the Far East - USWC trade and anticipates what it could mean for the coming months.

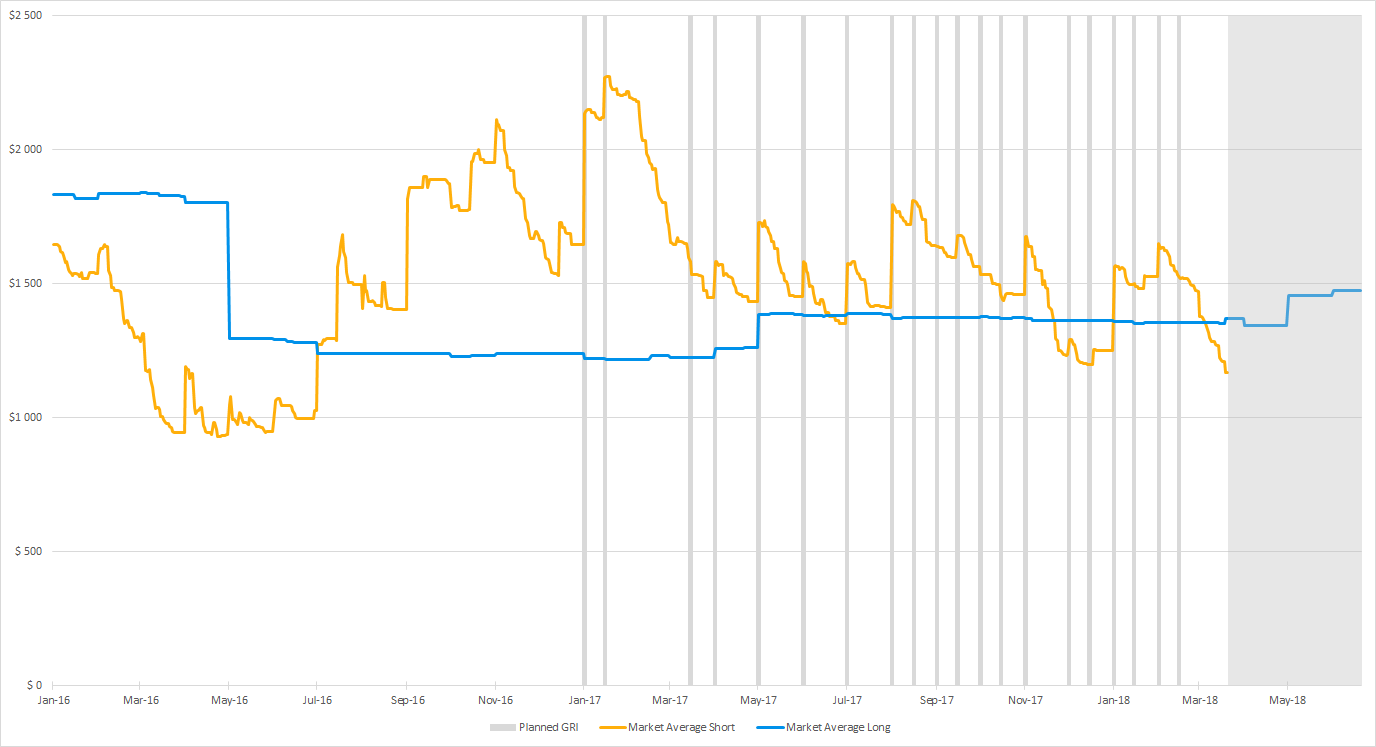

During 2017 carriers continued in their almost monthly ritual of announcing general rate increases (GRIs) on the Far East - USWC trade. At the turn of the year FAK increases of around $1,000 per FEU were partially adopted by the market, helping to increase rates from $1,646 FEU recorded on 31st Dec-16 to $2,134 FEU on 1st Jan-17, an increase of 29.6%. Building on this momentum and the rush to fulfill shipments prior to Chinese New Year (CNY) on 28th Jan-17, carriers implemented a second GRI in the same month, this time of around $600 per FEU, increasing rates to $2,269 FEU as reported on 15th Jan-17.

However, reflecting a key theme on many of the major trades, which we will explore for 2018, carriers were unable to maintain rate levels after the implementation of these GRIs. Once the market returned from CNY celebrations, rates begin to immediately slide, falling for the rest of Q1-2017. As of 31st Mar-17 they were reported at $1,447 FEU, some 32.2% lower than the start of the year.

During the remainder of 2017 rates subsequently failed to reach the high reported at the start of the year, despite carriers best efforts to push through multiple additional increases.

As we approach the end of Q1-2018, rates so far tell a very similar story the pattern witnessed in 2017. Carriers were again able to push through a planned GRI effective 1st Jan-18, this time for around $1,000 FEU. This helped to lift rates from $1,249 FEU on 31st Dec-17 to $1,565 FEU on 1st Jan-18, a jump of 25.3%.

Carriers once more capitalised on the pre-CNY rush, which fell slightly later in 2018, by implementing a further increase on 1st Feb-18, increasing rates to $1,648 FEU. However, since the start of February rates have trended downwards, falling by 29.1% to $1,169 FEU as of 20th Mar-18.

Related reading: How Chinese New Year 2018 Affected Container Rates (Historical Comparison)

Key Takeaways Offered From Understanding Recent Rate Developments

Shippers should be somewhat buoyed by carriers inability to sustain rates after GRIs have been implemented. This was a key trend in 2017 and seems to be repeating itself so far in 2018.

For example, a planned GRI was behind every noticeable rate increase of 2017, but in each case these were met with rate discounts within a week or less.

Image: Xeneta Platform

While historical rate developments are not necessarily reflective of how they may develop in the future, they remain indicative of a market which remains oversupplied and understanding these trends can provide a useful benchmark when negotiating long term contracts.

For example, in 2017 the average FAK rate for the full year was reported at $1,600 FEU. With hindsight shippers negotiating long term contacts were, on average able to achieve a discount to this.

Of course, carriers have the power to change market fundamentals via service withdrawals, but the discipline required for this to be sustained in the long run seems lacking. Therefore it’s not unreasonable to assume future GRIs on the trade, will on average, be quickly followed by rate discounting.

Despite this, early indications suggest some shippers are paying a premium to what could have been achieved in 2017. In particular, those negotiating long term contracts for commencement around May-18 are achieving an average price of $1,455 FEU, versus $1,386 FEU recorded at the same period a year earlier.

However, shippers should be questioning, with current FAK rates seemingly developing along the lines of 2017 and already 23.8% lower than this time last year (as of 20th Mar-18), should they be finalising long term contracts at a similar level to 2017 or perhaps slightly lower?