The winds of change may be blowing in the ocean freight market, albeit with just a gentle breeze (for now), as spot rates between the Far East and North Europe move above long-term contracted prices. Xeneta’s data suggests long-term rates may have bottomed out, giving shippers food for thought when it comes to timing the next round of contract tenders.

GRIs slightly slip, but still exert impact

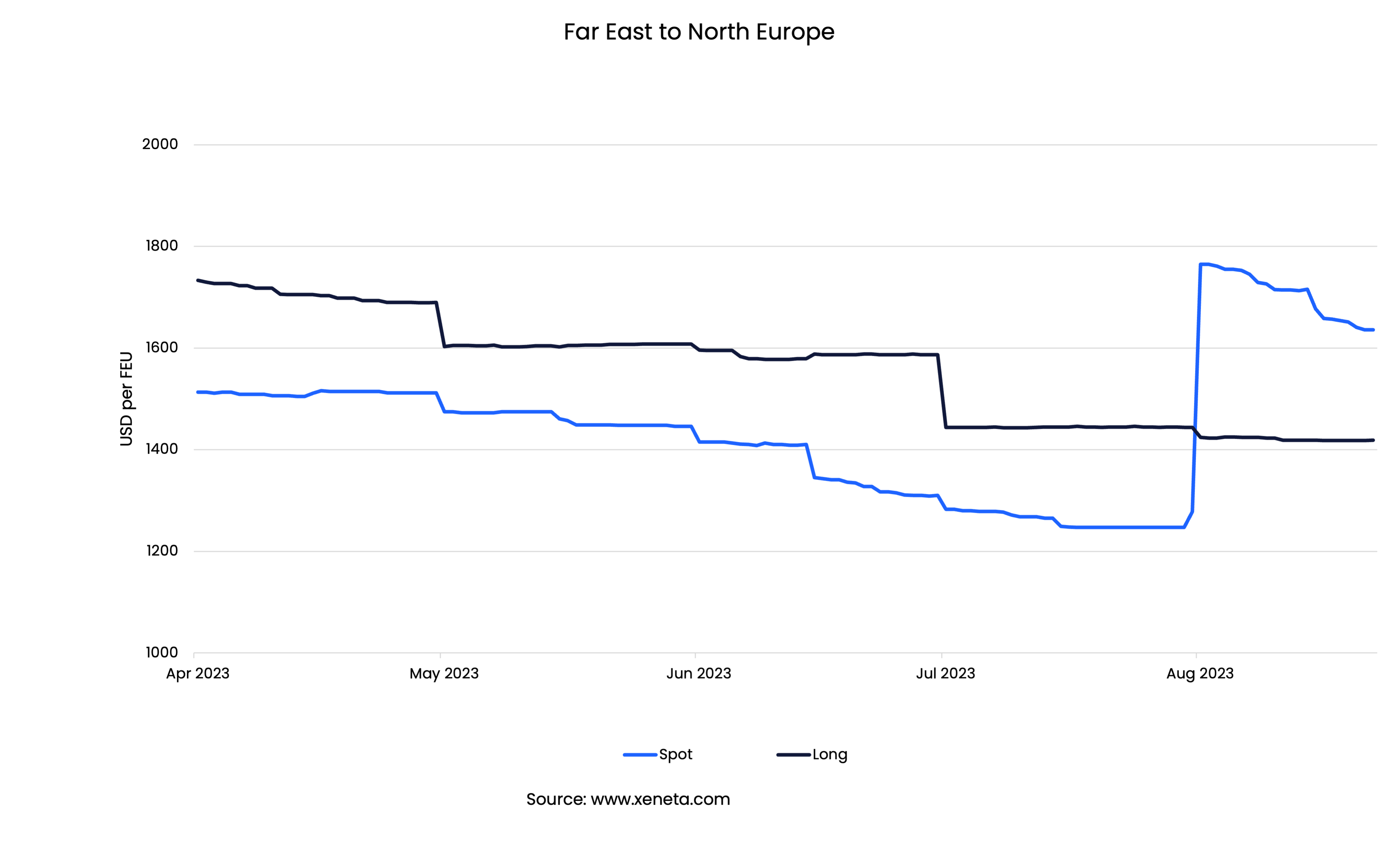

The initially successful early August GRIs between the Far East and North Europe are showing signs of losing some ground, with spot rates down around USD 100 per FEU from the start of the month. However, and especially given the context of earlier GRI moves this year, they have given rates a long sought after shot in the arm, with prices currently at USD 1 680 per FEU (more than a third higher than they were at the end of July).

This increase in rates also means that, for the first time since early August last year, spot rates are now higher than long term rates. Back then long-term rates stood at USD 9 100 per FEU, whereas today’s average is just USD 1 400 per FEU. Spot rates now command a premium of around 20%.

Wake-up call

Shippers, who until just a few months ago were looking to delay securing long term contracts in favor of cheaper spot rates, now face a new reality… and a new impetus to consider strategies.

Put bluntly, the sudden turnaround of the spot market should be a wake-up call to those shippers who were expecting rates to simply keep falling.

Bottoms up?

Looking at the average rate for long-term contracts signed within the past three months, the news is still positive for shippers. The rate fell again this month and on the 21st of August stood at USD 1 400 per FEU, the lowest it has been since September 2020. However, hiding slightly deeper in the data are clear signs that the party could be coming to an end.

The average rate for new long-term contracts signed within a month, rather than the average signed in the past three months, is no longer falling. August is the first time since April that there has been a month-on-month increase in the average rate of new contracts signed. Though small, the USD 30 per FEU increase in the average rate for new long-term contracts from the Far East to North Europe suggests rates have bottomed out and will soon start following spot rates upwards.

Historical perspective

The last time spot rates fell below long-term rates was in October 2019. As is the case now, GRIs then brought spot rates back up in November. Long-term rates stayed relatively flat for two months, before rising by USD 250 per FEU on the 1st of January. This is by no means a development and timeline that can be guaranteed this time round, but it’s not a development forward thinking shippers should ignore either.

These considerations are not only relevant between the Far East and North Europe – it’s a pattern we’re seeing on other major trades as carriers try to shore up the market before entering the next round of contract negotiations. So, as of today, long-term contracts are increasingly the cheaper option when compared to spot rates. Which begs the question – if there is clear potential for them to increase in coming months is it time to for shippers to strike when the iron is hot; locking in contracted rates while they’re still near the bottom? For many that might sound like a top idea.

Want to learn more?

Contact us to learn how Xeneta can help you prepare for this upcoming tender season and supplier/buyer negotiations. Gain the upper hand with actionable real-time ocean and air freight rate and capacity data.