-1.jpg)

While what we are all seeing in the news is terrible, what’s even worse is what we don’t see – which is how world trade is becoming paralyzed. 95% of the world’s trade is carried by container vessels and bulkers, or ‘was carried’ by container vessels. Sea Intelligence reported last week that 384 sailings have been blanked as of April 11.

The blankings are reflected in port volumes; Los Angeles Port moved 31% less TEU’s in March (YTY), their lowest volume since 2009’s Great Recession. America’s National Retail Federation just forecast a sustained reduction in container import volumes; predicting import TEU volume will be down (YTY) some 20% monthly April-July, with August expected to be -13% .

When coupled with last week’s U.S. Department of Commerce reporting an 8.7% drop in retail sales, along with the 22+million Americans unemployed in just the past four weeks, it’s frustrating that the only defense against the virus is to shut down the world’s economies.

American Ports Slow Down

While not exactly newsworthy, this slowdown is evident in America’s ports as they begin to adjust as to the new-norm of reduced TEU’s. Last week the Port of Virginia announced the temporarily closing its Portsmouth Marine Terminal, while other terminal operators in such major ports as Miami (POMTOC terminal), Seattle (SSA Marine-Terminal 18), and Baltimore (Seagirt Marine Terminal) have implemented shorter-duration closures. Additionally, multiple North American seaports have introduced rolling gate closures, reducing hours and work days at individual terminals in order to balance capacity with the now- reduced TEUs.

Last week Alphaliner reported that blanked sailings have laid up some 13% of the world’s container fleet, or approximately 3 million TEU’s. This is means the top 15 box carriers will suffer a loss of U.S.6 billion in revenue, says Sea-Intelligence, who added that an accompanying collapse in box rates could cause the carriers to lose $ 23.4 billion this year.

That collapse may be upon us On April 6, Rodolphe Saadé, CMA CGM’s CEO told French newspaper Le Figaro he expects May to be the slowest month to-date for box movements “We are estimating a 30% drop in global shipping.”

Sea Intelligence, Alphaliner, and Mr. Saade ’are not being dramatic on the slowdown of the economy.

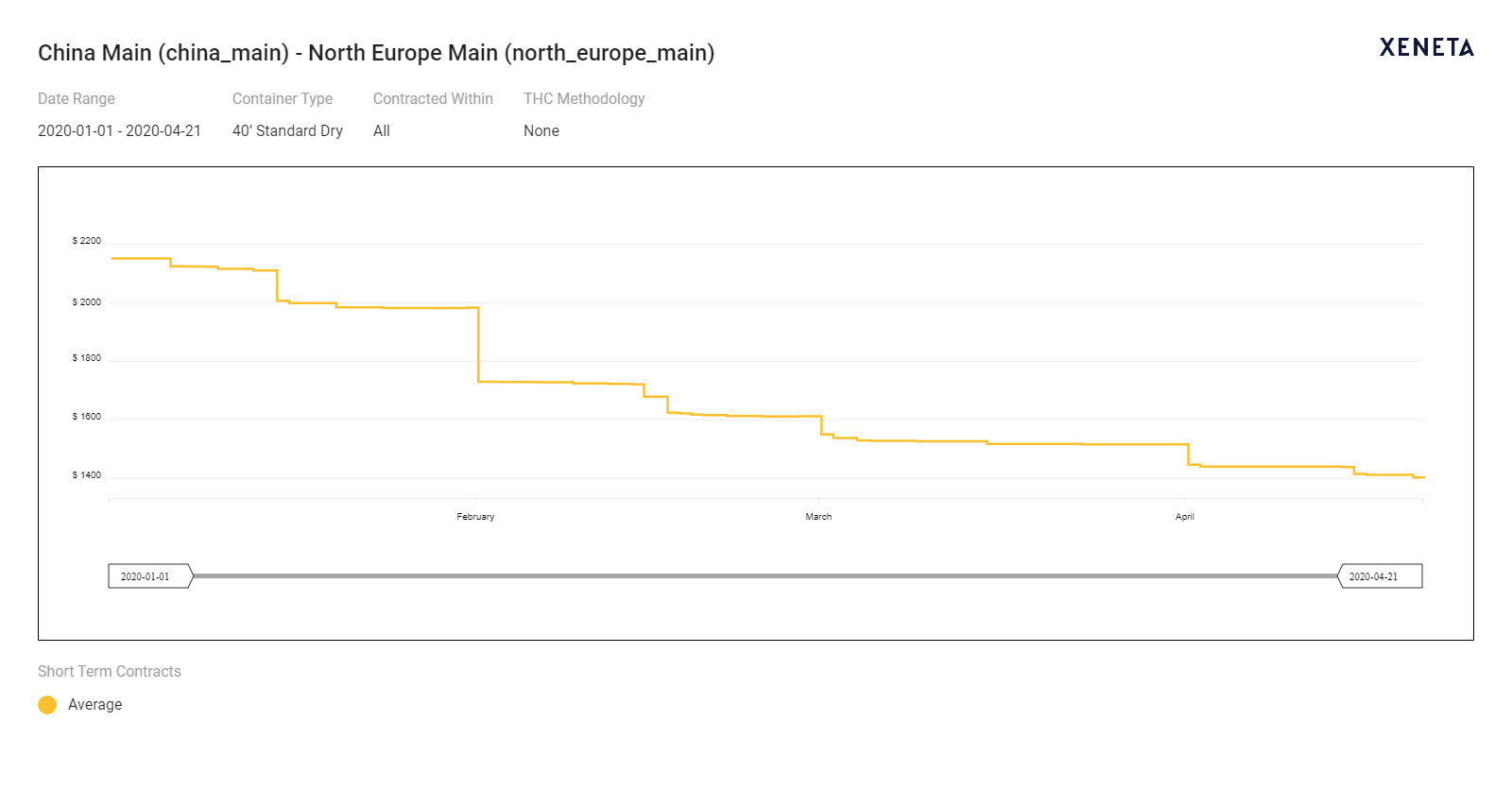

Our platform shows a USD748 drop in the short-term market average rate for the China Main- North Europe trade corridor from Jan 1 - April 21. See the chart below.

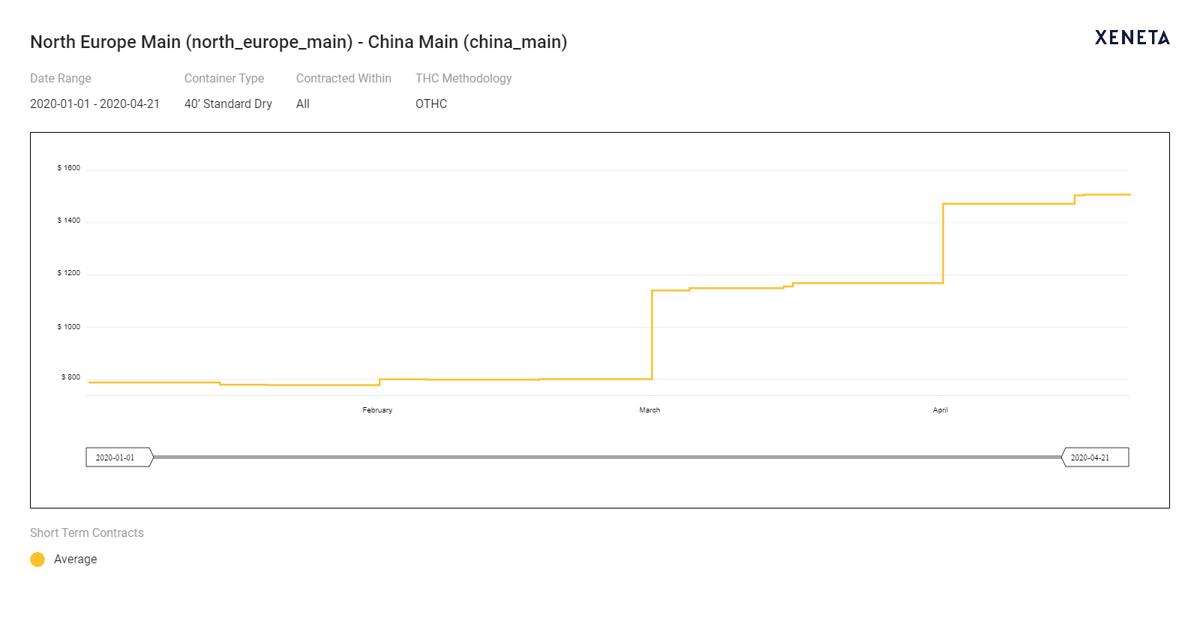

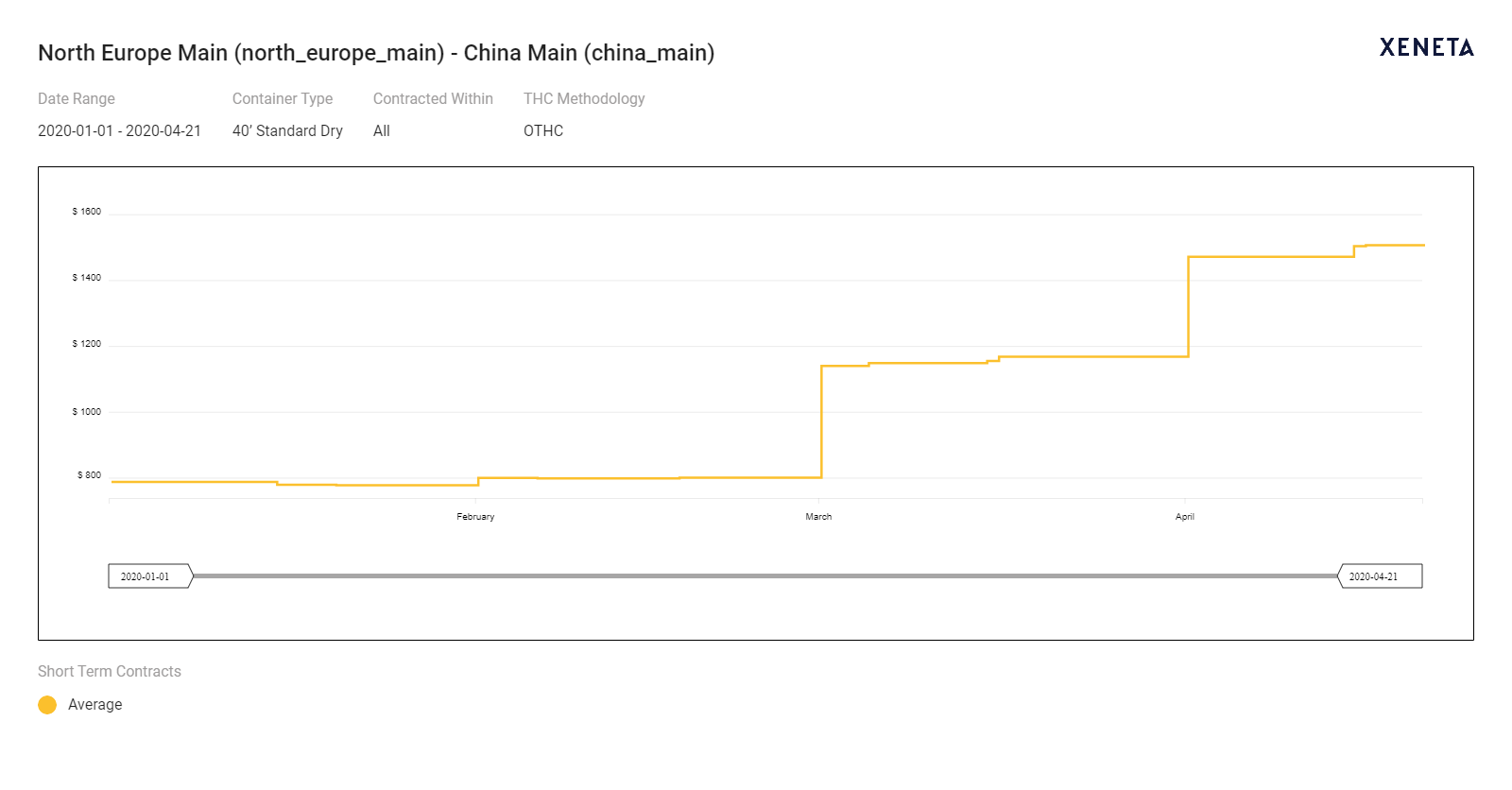

Now, what is more interesting is the tick up in rates for the North Europe to China Main trade. Xeneta has recorded a whopping increase of USD 720 for the same period, 91%. See the chart below.

Now, what is more interesting is the tick up in rates for the North Europe to China Main trade. Xeneta has recorded a whopping increase of USD 720 for the same period, 91%. See the chart below.

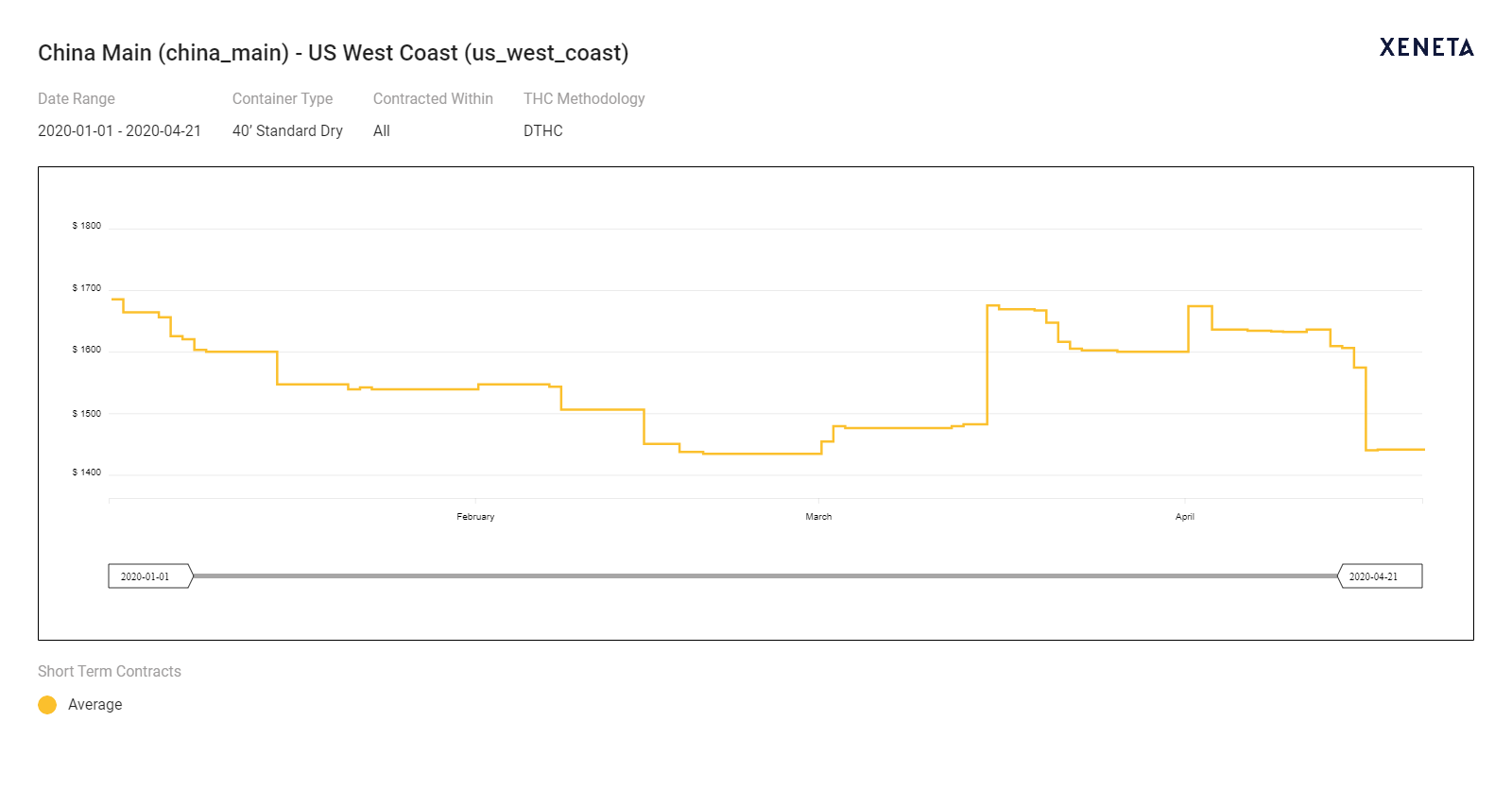

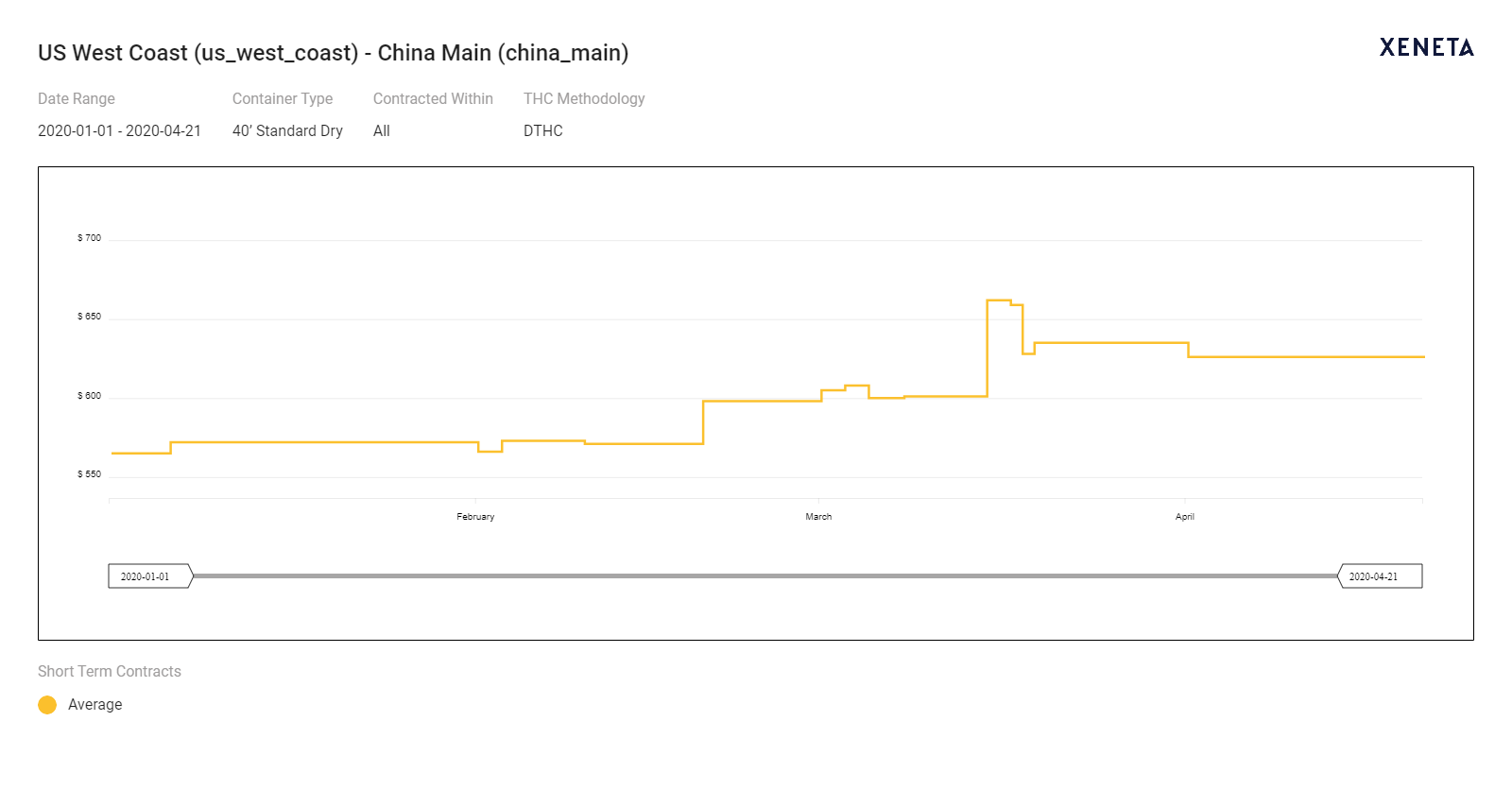

Our platform shows a USD244 drop in the short-term market average rate for the China Main- US West Coast trade corridor from Jan 1 - April 21. See the chart below.

Again, what is more interesting is the tick up in rates for the US West Coast to China Main trade. Xeneta has a small increase of USD 62 for the same period, 10%. See the chart below.

Again, what is more interesting is the tick up in rates for the US West Coast to China Main trade. Xeneta has a small increase of USD 62 for the same period, 10%. See the chart below.

The up-tick in Europe and US to China rates our platform reports is more a function of the container imbalance, as opposed to demand.

While shippers and carriers accept the cycle of rates and volume rising and falling almost never has the box industry seen such a collapse of TEU volumes and a yo-yo of rates. It's challenging to try to make sense of it. In March, Moody’s downgraded the credit outlook for Hapag-Lloyd, Maersk, MOL and NYK from ‘stable’ to ‘negative’ and placed CMA CGM’s credit ratings under review for potential downgrades.

Carriers with high levels of short term debt due 2020-2021 are especially vulnerable, and Alphaliner further warned of the eleven carriers surveyed, six (CMA CGM, Hapag-Lloyd, HMM, PIL, Yang Ming, Zim) have negative working capital.

While PIL continues to deny bankruptcy rumors, HMM has its own issues; our friends at Loadstar reported HMM’s new 24,000TEU flagship HMM Algeciras will be making her maiden voyage this week, on their just-postponed FE4 loop, meaning she has the possibility of being laid up immediately thereafter. Unfortunately, HMM has11 more 24,000 TEU megas joining the fleet between now and September, thus adding 288,000 TEU’s into a market for which there is no need for one more mega, much less 12.

One wonders to where will the existing TEU’s be cascaded, or will they be laid-up, generating no revenue? Be it individual, retail, or supply chain, this doesn’t look like it’s going to get better any time soon.