There are many topics of interest to the carriers, shippers, bunker suppliers, forwarders, BCOs, and others in the box industry. Still, today's plummeting box rates are the subject of most significant interest.

A look at our platform or any of the other container rate indexes might make the reader think the collapse in box rates is threatening the industry. But a step back might be in order; it's worth remembering that rates are cyclical, and maybe the slide in box rates is the same sort of correction that so commonly affects commodity prices and stock markets.

It is worth remembering that the volumes of cargo are still far above pre-Covid levels. The American West Coast Port of Long Beach just reported a near-record August 2022; they were only 764 TEUs (0.10%) short of August 2021, which was their busiest August on record.

Despite losing substantial vessels to the USEC ports due to port congestion, causing an import decline exceeding 5%, exports were up 1.6%, and empties increased 7.2%.

Overall, the Port of Long Beach said they've broken cargo records in six of the last eight months; Long Beach is up 4% in the eight months January – August 2022 vs. 2021.

Also, let’s not forget that the Port of Long Beach and LA were recently named second and third in cargo volume as more trade moved away from the West Coast due to ongoing concerns about labor strikes and lockouts.

But taking our focus back to the USWC, a look at our platform might be constructive:

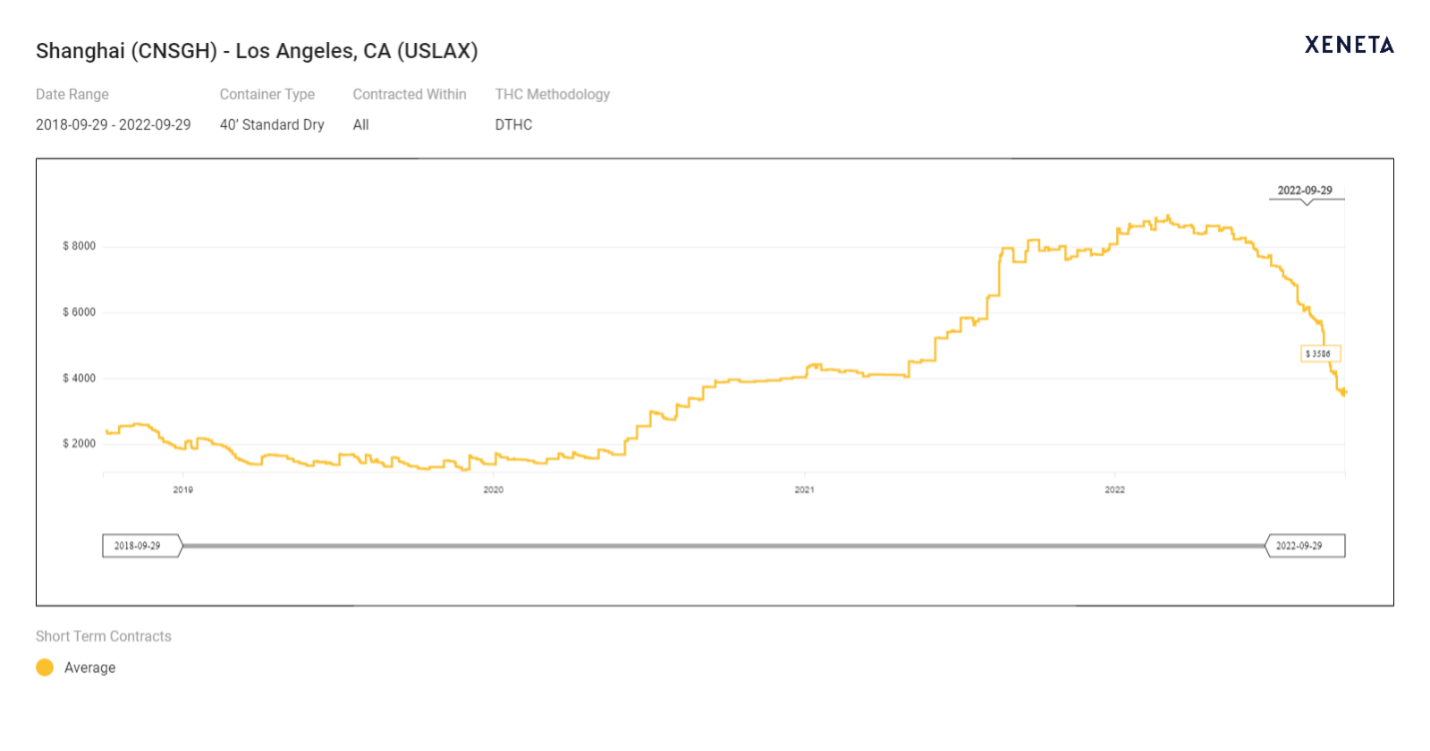

Short-term rates, 40' dry box, no surcharges, Shanghai – Los Angeles ports:

- Sept 24, 2022: US$ 3,764

- Mar 24, 2022: $ 8,787/ (6 months ago)

- Sept 24, 2021: $ 7,964 (12 months)

- Sept 24, 2020: $ 3,874 (2 years and in the depths of the Pandemic)

- Sept 24, 2019: $ 1344 (pre-pandemic)

Does this mean rates are headed to, or under, those pandemic years?

Does this mean rates are headed to, or under, those pandemic years?

They might overshoot on the downside if this 'correction' continues unabated before finding a more steady and higher level when the 'fire sale' is over.'

Not necessarily! Volumes of boxes carried are still healthy, large-scale blank sailings are yet to be announced outside of the inbound North American service network, and worth remembering there are far more box carriers carrying far more TEUs than ever.

Most carriers have large amounts of TEUs locked in on long-term contracts at far higher than current spot prices.

The carriers have yet to balance capacity/TEU's/sailings as they so ruthlessly did in Q2 2020. During that time span, they blanked and idled sufficient voyages and ships that enabled them to balance the demand against shipping capacity and then kept the demand-supply ratio in their favor. Not only did they stop the collapse of box rates, but they were able to orchestra capacity management to the degree that led to those multiple quarters of record profits.

Platts/American Shipper reported a few weeks ago that 'sources' told Platts they're looking to China's Golden Week holiday (Oct. 1-7) as a possible floor for box rates. Market participants are "bracing for a blank sailing program to be announced by carriers," Platts said.

However, a decline in spot rates does not have the same effect on ocean carrier financials as it did pre-pandemic because of the rise in the use of long-term contracts to make good movements on global supply chains more resilient.

Carriers today have far more of their volume on long-term contracts instead of multiple spot contracts and at far higher than spot rates. Zim recently said the rates in their 2022 contracts were 2x higher than 2021 rates, while Maersk revealed they have 71% of their TEUs contracted for 1+ years now, compared to 46% in 2019.

While some contracts are expected to be renegotiated as spot rates drop, the remaining high-priced contracts will more than balance the lower-priced spot transactions. Thus, not only do spot rates still have a long way to fall before they're back where they started — even at the steeper-than-expected pace of decline — they're also overshadowed by contract rates when it comes to near-term carrier profits.

However, there is no doubt that carrier and big volume-shipper dynamics will become difficult if the short-term market continues to decline. How difficult? We don't know. Relationship building on both sides of the table will be ever more important.

Multiple global economic issues need to be resolved for box rates to stabilize. The effect of the US Federal Reserve interest rate increase is unknown on the US economy.

The US Dollar is at record levels against most currencies, which could serve to cause global shipments to America to remain strong, thereby helping box rates to stay strong. American consumers historically shop the world out of a slow economy; a strong USD will help that to continue. Will Beijing's Zero-covid policy and lockdowns continue in those important export centers while continuing to stifle their domestic economy?

The UK continues to wobble; they have yet to resolve the trade issues caused by Brexit, and now their consumers are bedeviled by huge energy bills, rising food prices, and strikes at their two largest ports. EU energy prices have not yet been reflected in retail sales but should the Ukraine-Russia war spiral out of control; the EU will be the first affected.

And most important is the 7 million TEUs of new capacity beginning to arrive next year. Then we'll see if capacity management can stave off a more permanent rate decline.

Want To Get Your Hands On More Timely Insights?

Schedule a personalized demo of the Xeneta platform tailored to match your container shipping and air cargo procurement strategy.