In this month's newsletter, you will find a sneak peek into the latest Xeneta Shipping Index (XSI®) report and State of the Market webinar, which includes expert insights on what you need to know to stay on top of this key tender season.

In a recent turn of events, the congestion around the main terminals in the UK continent/North Europe is causing fear for all carriers, forwarders and shippers.

On the US East Coast, congestion has ticked up again in late August as shippers in North America shy away from the potential on the US West Coast while waiting for contract negotiations to finalize.

Keep reading for detailed insights,

What's new?

State of The Ocean Freight Market | On-DemandWebinar

Congestion Keeps Rates from Falling - Here’s what you need to know to stay on top of this key tender season

With spot rates falling below the long-term contract rates, shippers have a lot to think about while negotiating their long-term contracts.

Should they hold a renegotiation clause in their long-term contracts that they signed perhaps a quarter or a year ago with their main carriers? Would that allow them to strike a new deal? Do they need to bring something special to the negotiation table if they want lower rates?

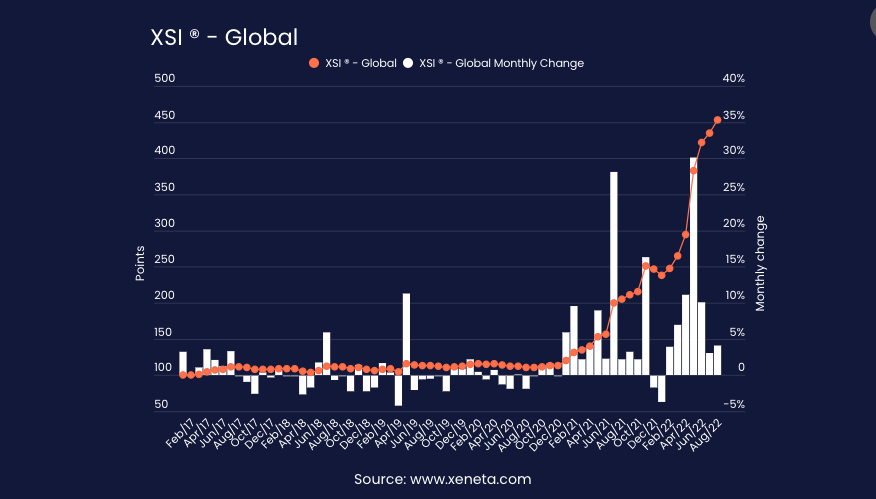

Despite softening spot rates, uneven demand and ongoing supply chain issues, the world’s leading carriers remain on course for another bumper year of profits. New long-term contracted rates are dropping on key trading corridors, following on the heels of declining spot prices.

However, since they’re replacing expiring agreements with considerably lower rates, the average paid by all shippers is still climbing.

The question is, for how long?

“There’s no doubt the major carriers have had it their way in negotiations for some time,” notes Patrik Berglund, Xeneta CEO. “The spectacular results they saw in 2021 will no doubt be repeated, and even bettered, this year, as seen by the huge profits that defined many Q2 financial reports. But there is a sense that change is in the air.”

Due to a lack of transparency, the total price to ship freight is never straightforward, as no one knows how carriers calculate the surcharges. Until now!

At Xeneta, our main aim is to provide data-driven transparency to the shipping industry with as much granularity as possible in the total price our customers pay. That's why we are excited to introduce our latest product update to our customers - Ocean Surcharge Dataset.

The detailed breakdown of total freight costs will allow our customers to find more cost-efficient routes, steer negotiations with a clearer market picture, and identify if their current surcharges line up with the market average.

Perhaps forgotten as the box carriers and shippers concentrate on US/EU port congestion, trucker strikes, and the Covid outbreaks that continue to bedevil China are bunker prices.

With the price of crude oil, natural gas, and LNG skyrocketing following the Russian invasion of Ukraine, bunker prices seem to have taken a back seat to the myriad of more pressing issues.

Progress on cutting emissions in container shipping has been moving at a tortoise pace. Many put it as "a lot of talks, but no action.

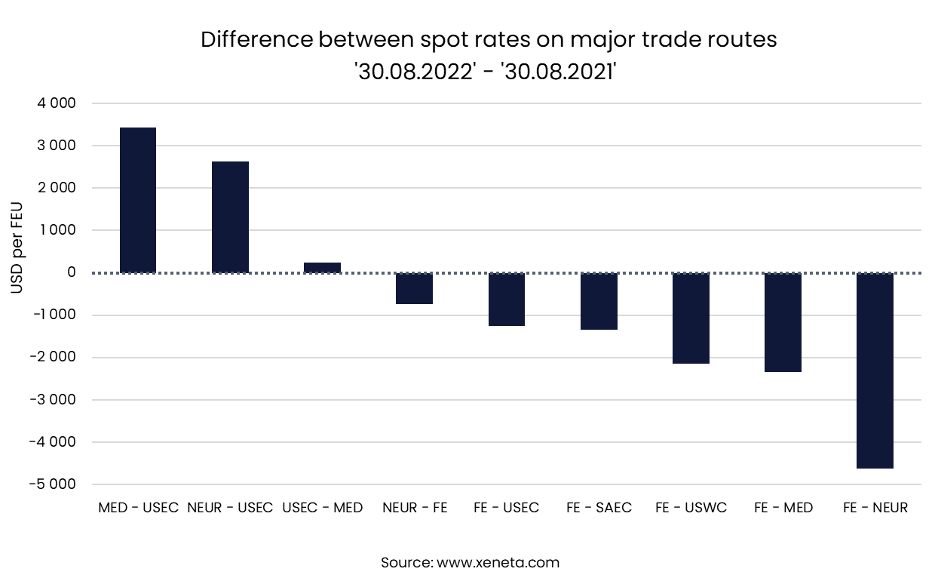

The recent trend of falling spot rates has left many shippers and the wider container shipping industry pondering how much it has fallen from last year until this summer. Despite the fall in spot rate over the summer, they are still much higher than a year ago on some major trades.

Out of Xeneta’s top 13 container trades, we selected only 9 to conduct this analysis as the remaining four trades had less than 10% YoY growth. For example, no change in spot rate difference occurred for the US West Coast to Far East route, which remained at USD 1 250 per FEU.

.png?upscale=true&width=1200&upscale=true&name=Leads%20Newsletter%20(7).png)

.png?upscale=true&width=1200&upscale=true&name=Live%20Product%20Demo%20Ads%20Q1%202022%20(2).png)